0% read

마지막 업데이트:

Joe Biden’s Views on Cryptocurrency

조지프 로비네트 바이든 주니어(Joseph Robinette Biden Jr., 1942년 11월 20일 출생)는 미국의 정치인으로, 제46대 미국 대통령입니다. 민주당 소속이며, 이전에는 버락 오바마 대통령 밑에서 2009년부터 2017년까지 제47대 부통령을 지냈고, 1973년부터 2009년까지 델라웨어주를 대표하여 미국 상원에서 활동했습니다. [1]

조 바이든의 암호화폐 행정 명령

2022년 3월 9일, 조 바이든 대통령은 디지털 자산 정책에 대한 조율을 위해 다양한 연방 기관에 지시하는 오랫동안 기다려온 행정 명령을 발표했습니다. [2]

"디지털 자산과 관련된 많은 활동이 기존 국내 법률 및 규정의 범위 내에 있지만, 미국이 글로벌 리더였던 분야에서 디지털 자산 및 관련 혁신의 성장과 채택, 그리고 특정 주요 위험으로부터 보호하기 위한 일관성 없는 통제로 인해 디지털 자산에 대한 미국 정부 접근 방식의 진화와 조정이 필요합니다." - 조 바이든의 행정 명령

제2조. 목표. 디지털 자산에 대한 미국의 주요 정책 목표:

"우리는 미국 내 소비자, 투자자 및 기업을 보호해야 합니다. 디지털 자산의 고유하고 다양한 기능은 적절한 보호 장치가 마련되지 않은 경우 소비자, 투자자 및 기업에 상당한 재정적 위험을 초래할 수 있습니다. 충분한 감독 및 기준이 없는 경우 디지털 자산 서비스를 제공하는 회사는 민감한 금융 데이터, 고객 자산 및 자금과 관련된 보관 및 기타 계약, 또는 투자와 관련된 위험에 대한 공개에 대한 부적절한 보호를 제공할 수 있습니다."

제5조. 소비자, 투자자 및 기업 보호 조치:

"디지털 자산 및 디지털 자산 거래소 및 거래 플랫폼의 사용 증가는 사기 및 절도와 같은 범죄, 기타 법적 및 규제 위반, 개인 정보 보호 및 데이터 침해, 불공정하고 학대적인 행위 또는 관행, 그리고 소비자가 직면한 기타 사이버 사고의 위험을 증가시킬 수 있습니다. 디지털 자산 사용의 증가와 커뮤니티 간의 차이는 정보가 부족한 시장 참여자에게 불균등한 재정적 위험을 초래하거나 불평등을 악화시킬 수도 있습니다. 디지털 자산이 소비자, 투자자 또는 기업에 부당한 위험을 초래하지 않도록 하고 안전하고 저렴한 금융 서비스에 대한 접근성을 확대하기 위한 노력의 일환으로 보호 장치를 마련하는 것이 중요합니다."[2]

조 바이든 대통령의 행정 명령은 암호화폐를 다루기 위해 미국 금융 규정을 업데이트하는 데 중점을 두었으며, 특히 연방 기관에 암호화폐를 연구하고 규제하기 위한 새로운 규칙을 제안하도록 지시했습니다. [39]

2023년 부채 한도 협상 중 암호화폐 거래자들에 대한 언급

2023년 5월 21일, 일본 히로시마에서 열린 G7 정상회담에서 조 바이든 대통령은 공화당 지도부와의 부채 한도 합의에 반대 의사를 표명했는데, 이는 "부유한 탈세범과 암호화폐 거래자"에게 이익이 될 것이라고 주장했습니다. [3][4][8]

"분명히 말씀드리지만, 저는 거의 백만 명에 가까운 미국인들의 식량 지원을 위태롭게 하면서 부유한 탈세범과 암호화폐 거래자를 보호하는 합의에는 동의하지 않을 것입니다."[8]

암호화폐 거래자에 대한 보호 주장은 세금 손실 상쇄를 의미합니다. 암호화폐 세금 손실 상쇄는 투자자가 전체 세금 부담을 줄이기 위해 사용하는 전략입니다. 여기에는 암호화폐 이익으로 인한 자본 이득을 상쇄하기 위해 손실로 암호화폐를 판매하는 것이 포함됩니다. 손실을 주장하려면 자산을 판매해야 하며, 판매 전후 30일 이내에 유사한 자산을 구매하는 데 수익금을 사용해야 합니다. 이 메커니즘은 주식 및 기타 자산에도 사용할 수 있습니다. [3]

제안된 암호화폐 채굴 세금

조 바이든 대통령은 2023년 5월 2일 암호화폐 채굴 회사에 30%의 소비세를 부과할 것을 제안했습니다. [10]

"현재 암호화폐 채굴 회사는 지역 환경 오염, 에너지 가격 상승, 기후에 대한 온실 가스 배출 증가의 영향 등 다른 사람에게 부과하는 모든 비용을 지불할 필요가 없습니다. DAME 세금은 기업이 사회에 미치는 피해를 더 잘 고려하기 시작하도록 장려합니다."라고 대통령 경제 자문위원회(CEA)는 성명에서 밝혔습니다.[9]

보고서에 따르면 미국 내 암호화폐 채굴자들은 2022년에 비트코인과 이더리움 간에 약 5만 기가와트시의 전력을 소비했으며, 이는 텔레비전과 거의 비슷한 수준이며 가정용 컴퓨터보다 훨씬 많은 양입니다. [11]

제안된 세금의 일환으로 디지털 자산 채굴자들은 사용 전력량, 전력원(재생 에너지 여부), 관련 가치를 공개해야 합니다. 또한 낭비되는 천연 가스를 전환하는 것과 같이 오프 그리드에서 생성된 전력에도 적용됩니다.[11]

행정부는 환경 문제 외에도 디지털 자산 채굴이 오염으로 인해 유색인종 커뮤니티에 불균형적으로 영향을 미치고 재생 에너지 비용을 상승시킨다고 주장합니다. 또한 보고서는 암호화폐에 대한 가치 판단을 내립니다. [9][11]

"암호화폐 채굴은 유사한 양의 전력을 사용하는 기업과 일반적으로 관련된 지역 및 국가 경제적 이익을 창출하지 않습니다."라고 명시되어 있습니다. "대신 에너지는 더 넓은 사회적 이익이 아직 실현되지 않은 디지털 자산을 생성하는 데 사용됩니다."[9]

미국의 암호화폐 논쟁

상품선물거래위원회(CFTC)

2022년 1월 3일, 상품선물거래위원회(CFTC)는 **Blockratize, Inc.**에 대해 스왑 실행 시설로 등록하지 않고, 예측 시장 웹사이트 Polymarket에서 암호화폐를 사용하여 불법 바이너리 옵션 계약을 제공하고, 상품 거래법을 위반하여 베팅 시장을 폐쇄한 혐의로 140만 달러의 벌금을 부과하는 명령을 내렸습니다. [12]

"본 명령은 Polymarket이 140만 달러의 민사 벌금을 지불하고, 상품 거래법(CEA) 및 해당 CFTC 규정을 준수하지 않는 Polymarket.com에 표시된 모든 시장의 해결(즉, 정리)을 용이하게 할 것을 요구합니다."

CFTC의 발표에 따라 Polymarket은 다음과 같은 성명을 발표했습니다.

"CFTC와의 합의에 성공적으로 합의했음을 확인하게 되어 기쁩니다. 2022년 1월 14일 이후에 해결될 예정인 법을 준수하지 않는 세 개의 시장은 조기에 정리되고 참가자에게 환불될 것입니다."[12]

2022년 2월 9일, CFTC 위원장 Rostin Behnam은 미국 상원 농업, 영양 및 산림 위원회에서 증언하면서 비트코인과 같은 특정 암호화폐를 규제할 수 있는 권한을 미국 제117대 의회에 요청했습니다. [13]

2022년 6월 2일, CFTC는 암호화폐 거래소 Gemini의 경영진이 2017년에 회사가 제안한 비트코인 선물 계약의 시장 조작에 대해 규제 당국과의 소통에서 허위 및 오해의 소지가 있는 진술과 누락을 했다고 주장하며 Gemini를 상대로 소송을 제기했습니다. [14]

2022년 6월 7일, 미국 상원 의원 Kirsten Gillibrand와 Cynthia Lummis는 대부분의 디지털 자산을 CFTC의 감독을 받는 상품으로 취급하고 암호화폐 보유자가 기업 투자자와 동일한 권한을 갖지 않는 한 SEC의 감독을 받지 않도록 하는 암호화폐 규제 프레임워크를 만드는 법안을 발의했습니다. [15] 2022년 6월 8일, Behnam은 해당 법안에 대한 지지를 발표했습니다. [16]

2022년 6월 14일, The Wall Street Journal이 주최한 컨퍼런스에서 미국 증권거래위원회(SEC) 위원장 Gary Gensler는 Lummis-Gillibrand 법안이 주식 시장 및 뮤추얼 펀드 보호를 부주의하게 훼손할 수 있다는 우려를 표명하고, 암호화폐 회사가 이미 SEC의 감독을 받는 행위에 관여하고 있으며, 일부 디지털 자산은 상품이 아닌 SEC의 감독이 필요한 증권이라고 주장했습니다. [17]

연방준비제도

2021년 10월 14일, United Wholesale Mortgage는 비트코인으로 모기지 대출 상환을 받는 회사 시범 운영을 중단한다고 발표했습니다. [18]

“암호화폐 공간의 점진적인 비용과 규제 불확실성의 현재 조합으로 인해, 현재로서는 시범 운영을 넘어 확장하지 않기로 결론 내렸습니다.”라고 CEO Mat Ishbia가 말했습니다.

미시간에 본사를 둔 이 모기지 회사는 암호화폐 – BTC, 이더 및 도지코인 – 세 가지 유형과 여러 다른 차용자를 대상으로 프로세스가 어떻게 작동하는지 확인하려고 했습니다. UWM은 2021년 9월에 사상 최초로 암호화폐 모기지 결제를 성공적으로 수락했으며 10월에 5건을 더 수락했습니다. 그러나 궁극적으로 수요가 없었습니다. Ishbia는 CNBC에 차용자들이 “좋아했고” “멋지다고 말했다”고 말했지만 암호화폐로 거래할 수 있는 옵션이 있는 것이 “동기가 되지 않았다”고 말했습니다. [18]

2022년 7월 8일, 연방준비제도 부의장 라엘 브레이너드는 암호화폐 산업 규모가 금융 시스템을 위협하기 전에 암호화폐에 대한 더 큰 규제를 촉구했습니다. [19]

“혁신은 금융 서비스를 더 빠르고 저렴하며 포괄적으로 만들고 디지털 생태계에 고유한 방식으로 그렇게 할 수 있는 잠재력이 있습니다.”라고 그녀는 런던에서 열린 잉글랜드 은행 컨퍼런스에서 연설했습니다. “암호화폐 금융 시스템에 대한 건전한 규제의 기반이 암호화폐 생태계가 너무 크거나 상호 연결되어 광범위한 금융 시스템의 안정성에 위험을 초래할 수 있기 전에 지금 확립되는 것이 중요합니다.”[19]

법무부 및 국토안보부

2021년 3월 5일, McAfee Corp.의 설립자인 존 맥아피는 자신의 트위터 계정에서 암호화폐 펌프 앤 덤프 계획을 홍보하여 2,300만 달러를 벌어들인 혐의로 뉴욕 남부 연방 지방 법원에 기소되었습니다(이전 10월에 해당 계획으로 얻은 돈에 대한 탈세 혐의로 법무부에 의해 기소되고 SEC에 의해 홍보 혐의로 고소된 후)[20]

“맥아피 팀 구성원들은 알트코인 스캘핑 활동으로 총 2백만 달러 이상의 불법 이익을 얻었습니다.”라고 법무부는 주장합니다. [20]

2021년 5월 13일, 바이낸스는 사용자들이 돈세탁 및 탈세에 사용하는 것으로 인해 미국 법무부 및 국세청의 조사를 받고 있는 것으로 보도되었습니다.[21]

"저희는 자금세탁 방지 원칙과 금융 기관에서 사용하는 도구를 통합하여 의심스러운 활동을 탐지하고 처리하는 강력한 규정 준수 프로그램을 구축하기 위해 열심히 노력했습니다."라고 바이낸스 대변인은 이메일에서 밝혔습니다.

2022년 2월 8일, 미국 법무부는 사업가 일리야 리히텐슈타인과 래퍼 헤더 R. 모건을 2016년 비트피넥스 해킹에서 도난당한 45억 달러 상당의 비트코인 중 36억 달러를 세탁하려 한 혐의로 체포하고 압수했습니다. 비트피넥스 플랫폼에서 도난당한 119,756 BTC 중 **미국 법무부(DOJ)**는 거의 94,000 BTC(회수 당시 약 36억 달러 상당)를 회수했습니다. 리사 모나코 법무부 차관은 성명에서 이것이 *“법무부의 사상 최대 규모의 금융 압수”*라고 밝혔습니다.[22]

2022년 5월 6일, 미국 법무부는 Mining Capital Coin (MCC)의 CEO를 6,200만 달러 규모의 사기적인 암호화폐 계획을 운영한 혐의로 기소했습니다.

“암호화폐 기반 사기는 악의적인 행위자들이 투자자를 속이고 합법적인 기업가들이 이 신흥 공간 내에서 혁신할 수 있는 능력을 제한함에 따라 전 세계 금융 시장을 훼손합니다.”라고 법무부 형사부의 케네스 A. 폴라이트 주니어 차관보는 말했습니다.

기소장에 따르면 MCC의 CEO이자 설립자인 카푸치는 MCC의 소위 “거래 봇”을 투자자들이 암호화폐 시장에 투자할 수 있는 추가 투자 메커니즘으로 홍보하고 사기적으로 마케팅했습니다. 카푸치는 MCC가 “아시아, 러시아 및 미국의 최고의 소프트웨어 개발자들과 협력하여 이전에 본 적 없는 새로운 기술로 테스트된 개선된 버전의 거래 봇을 만들었다”고 주장했습니다.[23]

2022년 5월 12일, EminiFX의 CEO인 알렉상드르는 뉴욕 남부 연방 지방 법원에서 5,900만 달러 규모의 사기적인 암호화폐 계획을 운영한 혐의로 연방수사국(FBI)에 의해 기소되었습니다. 알렉상드르는 체포되어 전신 사기 및 상품 사기 혐의로 기소되었습니다.[24]

"투자자들은 허위 주장과 벼락부자 계획의 단점 위험을 경계해야 하며, 종종 너무 좋아서 사실이 아닐 수 있습니다."라고 맨해튼의 데미안 윌리엄스 미국 변호사는 기소 발표 성명에서 말했습니다.

2022년 6월 3일, 연방거래위원회는 2021년 1월부터 2022년 3월까지 약 46,000명의 투자자가 암호화폐 사기로 10억 달러 이상을 잃었다는 보고서를 발표했습니다(2022년 1분기에 3억 2,900만 달러).[25]

2022년 6월 30일, 미국 법무부는 1억 달러 이상의 암호화폐 거래소 폰지 사기인 EmpiresX의 지도자들에 대해 증권 사기 혐의를 제기했습니다. 2022년 9월 8일, EmpiresX의 수석 트레이더인 조슈아 데이비드 니콜라스는 투자자로부터 약 1억 달러를 모은 글로벌 암호화폐 투자 사기 계획에 대해 유죄를 인정했습니다.[26]

2022년 6월, 미국 연방수사국(FBI)은 40억 달러 규모의 원코인 폰지 사기 사건으로 원코인 암호화폐 창립자 루자 이그나토바(일명 '크립토퀸')를 '10대 수배자' 목록에 추가했습니다. [27]

2022년 7월 21일, 전 코인베이스 직원 3명이 뉴욕 남부 지방법원에서 암호화폐 거래소에 상장된 150만 달러 상당의 암호화폐 자산과 관련된 내부자 거래 혐의로 기소되었습니다. 코인베이스의 전 제품 관리자였던 32세의 이샨 와히는 회사의 특정 디지털 토큰 제공 계획에 대한 기밀 정보를 그의 형제인 니킬 와히와 친구인 사미르 라마니에게 유출한 혐의를 받고 있습니다. [28]

“이번 사건의 혐의는 전통적인 금융 시장이 아닌 암호화폐 거래소에서 이루어진 거래와 관련되어 있지만, 여전히 내부자 거래에 해당합니다.” FBI 부국장 마이클 드리스콜이 성명에서 밝혔습니다.

재무부 및 노동부

2021년 8월 6일, 바이든 행정부는 미국 상원 의원인 롭 포트먼, 커스틴 시네마, 마크 워너가 제안한 인프라 투자 및 일자리 법안에 대한 암호화폐 세금 보고 수정안을 지지한다고 발표했습니다. 이는 미국 상원 의원인 신시아 루미스, 팻 투미, 론 와이든이 제안한 수정안보다 우선시된 것입니다. [29]

2021년 8월 9일, 투미, 워너, 루미스, 시네마, 포트먼이 제안한 타협안(No. 2656)은 투미 상원 의원이 만장일치 동의 투표를 요청했을 때 통과되지 못했습니다. 이는 리처드 셸비 상원 의원이 자신이 도입한 국방 인프라 지출 수정안(No. 2535)이 포함되지 않으면 해당 수정안에 반대했기 때문입니다. 투미 상원 의원은 이에 동의했지만, 버니 샌더스와 톰 카퍼 상원 의원이 반대했습니다. [30]

2021년 11월 15일, 바이든 대통령은 암호화폐 세금 보고 및 암호화폐 브로커 정의와 관련된 법안의 원래 문구가 포함된 인프라 투자 및 일자리 법안에 서명했습니다. 초당적 블록체인 코커스 의원들은 모든 하원 의원에게 보낸 서한에서 상원의 암호화폐 조항에 대한 우려를 제기했습니다. [31]

“변경되지 않은 이 조항은 우리나라의 암호화폐 투자자에게 광범위한 영향을 미치고 미국의 혁신을 더욱 규제할 것입니다.”라고 그들은 썼습니다. [31]

2022년 4월 20일, 미국 재무부는 2022년 러시아의 우크라이나 침공이 3개월째에 접어들면서 러시아 비트코인 채굴자들에게 제재를 가했습니다. [32]

BitRiver의 설립자이자 CEO인 Igor Runets는 “이러한 미국의 조치는 분명히 암호화폐 채굴 산업에 대한 간섭, 불공정한 경쟁, 미국 기업에 유리하게 글로벌 권력 균형을 바꾸려는 시도로 간주되어야 합니다.”라고 말하며, 회사는 “러시아 정부 기관에 서비스를 제공한 적이 없으며 워싱턴의 제재 대상이 된 고객과 협력한 적이 없습니다.”라고 덧붙였습니다.

2022년 5월 6일, 재무부는 Lazarus Group(북한 정부가 운영하는 사이버 범죄 조직)이 암호화폐 기반 게임인 Axie Infinity에서 훔친 것으로 알려진 2,050만 달러의 암호화폐를 세탁하는 데 사용했기 때문에 암호화폐 믹서인 Blender.io를 미국 금융 시스템에서 제재했습니다. 재무부의 보도 자료에 따르면 가상 화폐 믹서에 대해 제재를 가한 것은 이번이 처음입니다. [33]

증권거래위원회(SEC)

2023년 6월 5일, SEC는 암호화폐 거래소인 바이낸스와 CEO 창펑 자오를 바이낸스의 미국 법률에 대한 “노골적인 무시”라고 부르는 행위에서 비롯된 혐의로 기소했습니다. 136페이지 분량의 고소장에서 SEC는 바이낸스, 미국 계열사인 바이낸스.US 및 자오가 미등록 미국 금융 기관을 운영하고, 회사의 위험 통제에 대해 투자자를 오도하고, 거래량을 부풀리고, “수십억 달러의 투자자 자산”을 혼합하여 자오가 소유한 제3자 법인으로 보냈다고 주장했습니다. 이 사건은 미국 컬럼비아 특별구 지방 법원에 제기되었습니다. [37]

“자오와 바이낸스 법인은 광범위한 기만, 이해 상충, 정보 공개 부족 및 법률의 계산된 회피에 관여했습니다.”라고 SEC 의장 게리 겐슬러가 성명에서 밝혔습니다.

바이낸스는 바이낸스.US의 고객 자산이 위험에 처해 있다는 주장을 포함하여 SEC의 주장을 블로그 게시물에서 부인했습니다. 회사는 양측이 합의에 대한 논의에 참여한 후 SEC가 이 사건을 법정에 가져오기로 한 결정에 “낙담했다”고 말했습니다.

"SEC의 주장을 심각하게 받아들이지만, 긴급한 상황은 고사하고 SEC 집행 조치의 대상이 되어서는 안 됩니다. 우리는 우리 플랫폼을 적극적으로 방어할 것입니다. 불행히도 SEC가 우리와 생산적으로 소통하기를 거부하는 것은 위원회가 디지털 자산 산업에 절실히 필요한 명확성과 지침을 제공하기를 잘못 인도하고 의식적으로 거부하는 또 다른 예일 뿐입니다." - 바이낸스는 블로그 게시물에서 썼습니다.[38]

2023년 6월 6일, 미국 증권거래위원회는 중앙 집중식 암호화폐 거래 플랫폼인 코인베이스를 고소했습니다. 연방 규제 기관은 코인베이스가 암호화폐 자산 거래 플랫폼을 미등록 국가 증권 거래소 및 브로커로 운영했다고 주장합니다. [40] SEC는 또한 코인베이스가 고객에게 제공한 최소 13개의 암호화폐 자산(솔라나 및 카르다노 토큰 포함)이 고소장에 따라 “암호화폐 자산 증권”에 해당한다고 주장합니다.[41]

SEC 발표 후 트윗에서 코인베이스 공동 창립자 겸 CEO 브라이언 암스트롱은 다음과 같이 말했습니다.

“오늘 우리에 대한 SEC 고소와 관련하여 암호화폐 규칙에 대한 명확성을 얻기 위해 법원에서 업계를 대표하게 된 것을 자랑스럽게 생각합니다.”[42]

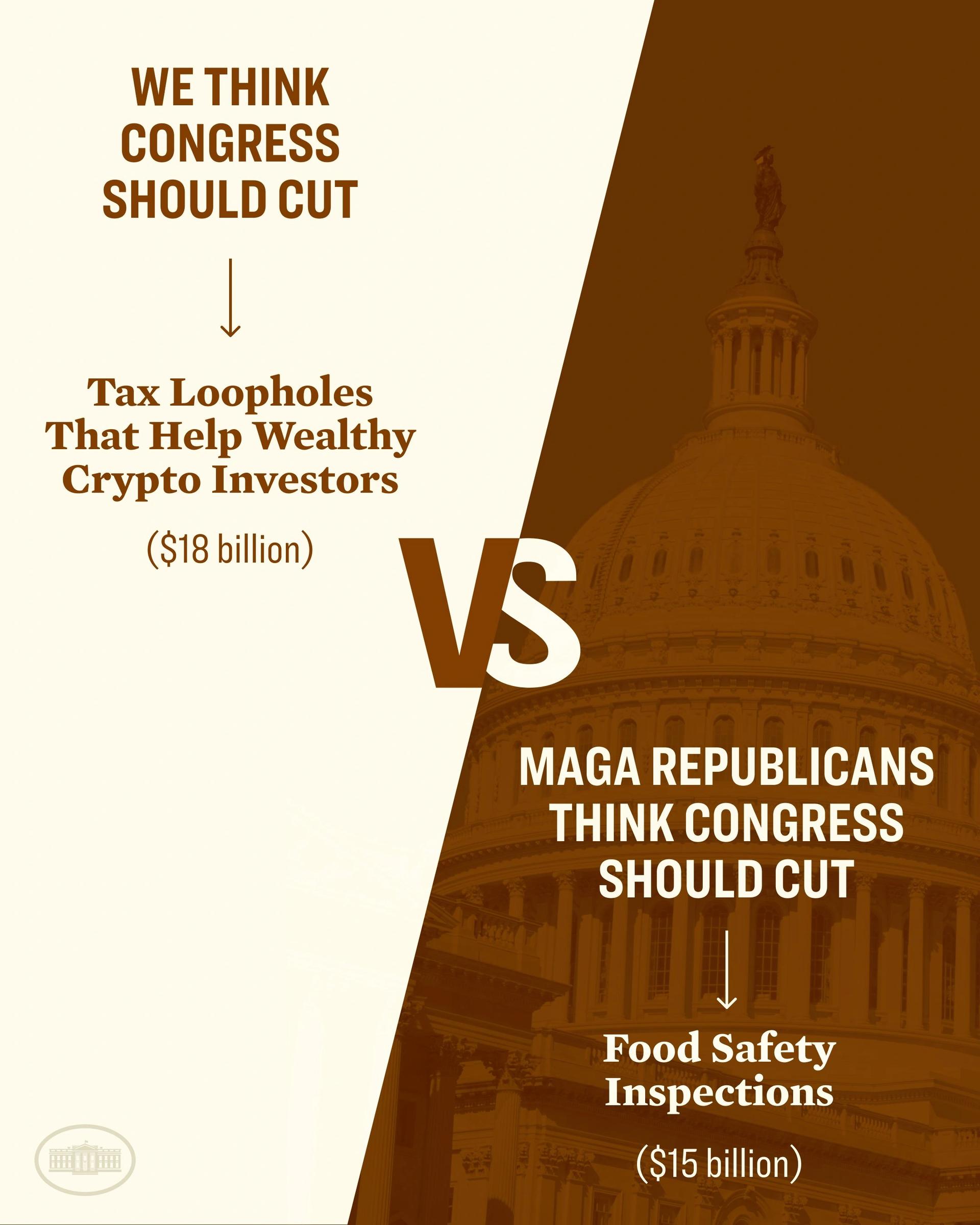

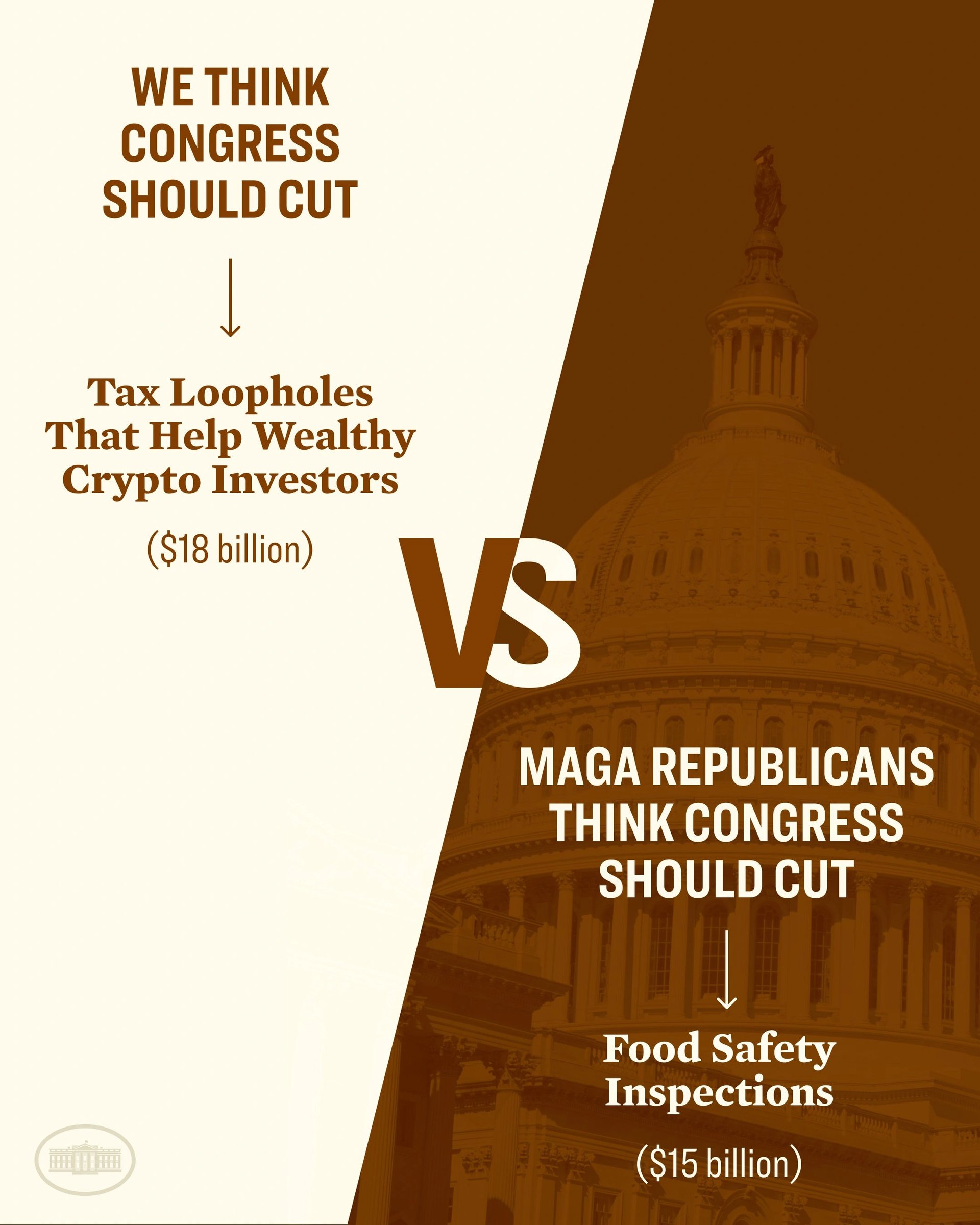

바이든, 180억 달러 규모의 '암호화폐 세금 허점' 종식 촉구

2023년 5월 9일, 조 바이든 대통령은 트위터에 인포그래픽을 공유하며 부유한 암호화폐 투자자들을 돕는다는 '세금 허점'을 없애야 한다고 주장했습니다. 커뮤니티 구성원들은 대통령이 공유한 수치와 해당 허점의 존재 여부에 대해 의문을 제기하며 트윗에 응답했습니다. [34][35]

도지코인 공동 창립자인 빌리 마커스도 바이든의 트윗에 답글을 달았습니다. 마커스는 어떤 허점이 존재하는지 물었고, 암호화폐로 번 돈보다 정부에 더 많은 돈을 냈다고 주장하며 '모든 위험을 감수했다'고 말했습니다. 그런 다음 대부분의 미국 암호화폐 사용자는 부자가 아니라 생계를 유지할 수 없기 때문에 암호화폐를 사용하려고 한다고 지적했습니다. [34]

조 바이든, 암호화폐 법안 거부

2024년 5월 31일, 조 바이든 미국 대통령은 SEC의 직원 회계 공보 121호를 폐지하는 하원 공동 결의안에 거부권을 행사했습니다. 비평가들은 이 공보가 암호화폐 기업이 은행과 협력하는 것을 어렵게 만든다고 말합니다. [43][44]

“이러한 방식으로 SEC 직원의 신중한 판단을 뒤집는 것은 회계 관행에 관한 SEC의 광범위한 권한을 약화시킬 위험이 있습니다.”라고 바이든은 백악관이 발표한 성명에서 밝혔습니다.[43] “우리 행정부는 소비자와 투자자의 복지를 위태롭게 하는 조치를 지지하지 않을 것입니다. 소비자와 투자자를 보호하는 적절한 안전 장치는 암호화폐 자산 혁신의 잠재적 이점과 기회를 활용하는 데 필요합니다.” - 그는 덧붙였습니다.

잘못된 내용이 있나요?

평균 평점

아직 평가가 없습니다

경험은 어땠나요?

빠른 평가를 해서 우리에게 알려주세요!

편집자

June 24, 2025. 12:29 UTC

편집 요약:

Add 'Government' tag and update content formatting.