0% read

Collateralization Ratio

Collateralization Ratio

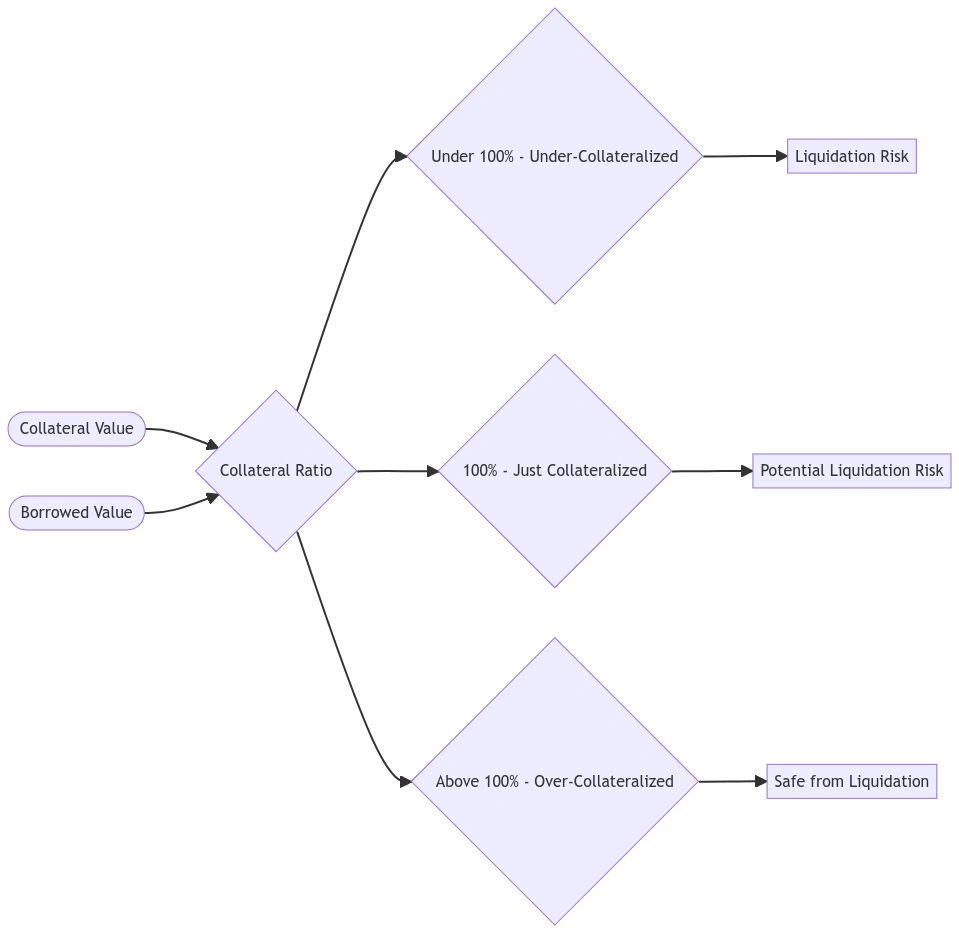

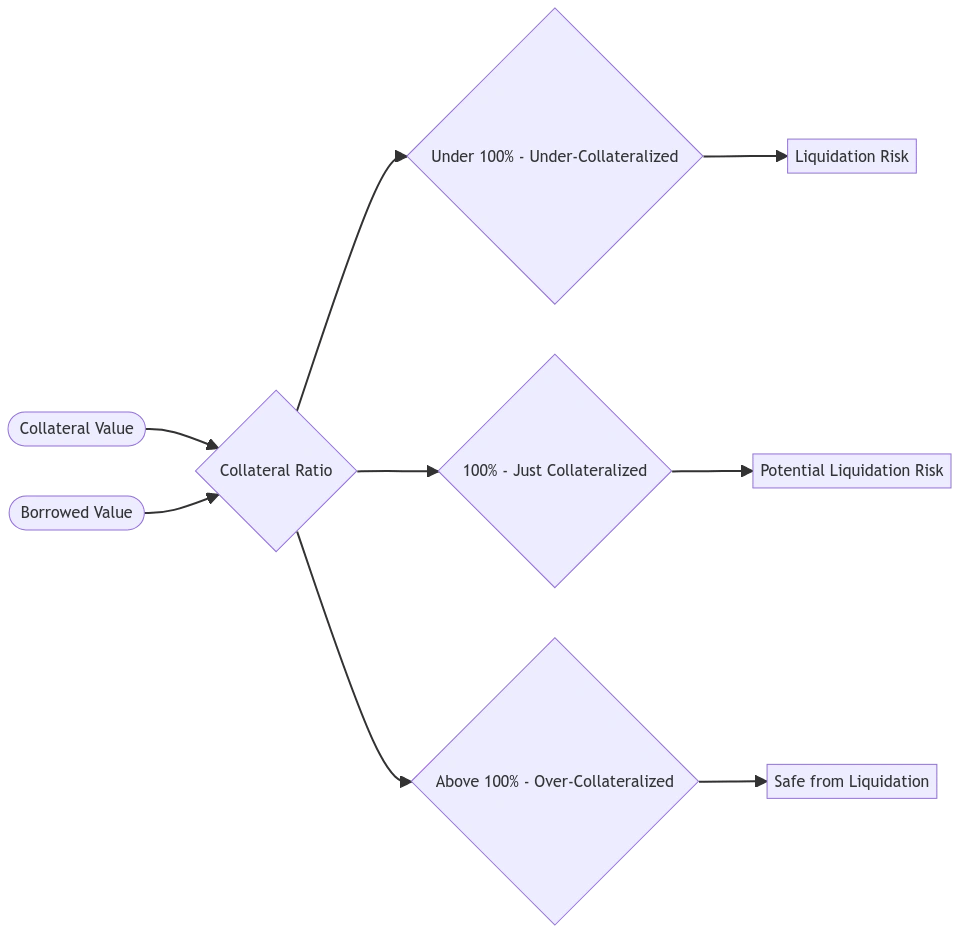

The collateralization ratio is an important metric in decentralized finance (DeFi) that signifies the financial stability of a position in any lending or borrowing scenario. It is calculated as the total collateral value divided by the total borrowed value and expressed as a percentage. A higher collateralization ratio indicates a lower risk for lenders, as they are protected from default by having possession of assets in case the borrower defaults.

Overview

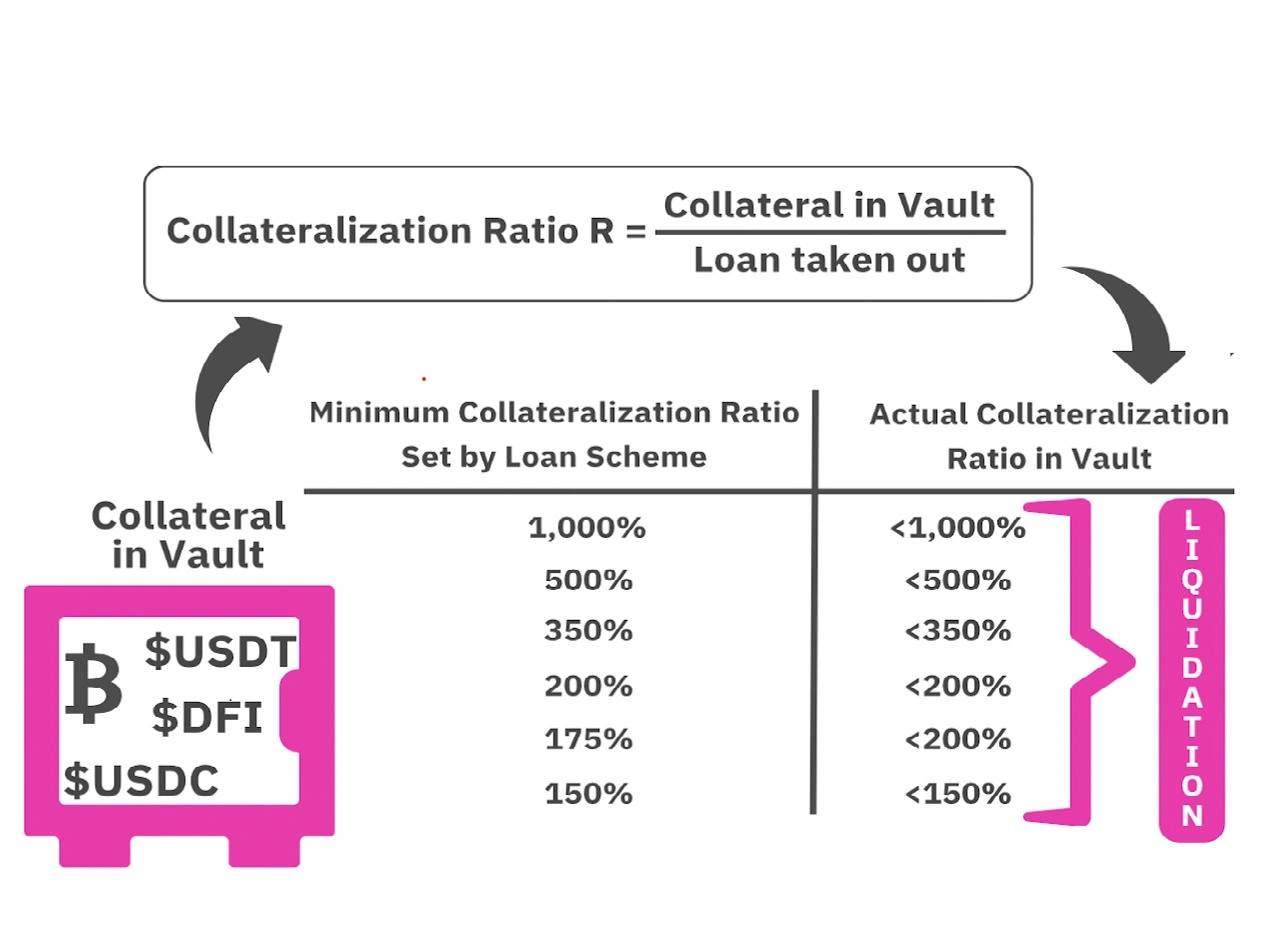

The collateralization ratio is a measure used to determine the percentage of a borrower’s total value of collateral relative to the amount they wish to borrow. It’s calculated using the following formula:[4] Collateralization Ratio = (Total Collateral Value / Total Borrowed Value) * 100%

This ratio is essential as it signifies the financial stability of a position in any lending or borrowing scenario, especially in the realm of decentralized finance (DeFi).[1]

Collateralization ratios can be different in centralized finance (CeFi) and decentralized finance (DeFi) systems. In centralized finance (CeFi), collateralization ratios are typically determined by traditional financial institutions such as banks and are often subject to regulatory requirements. These ratios may vary depending on the type of loan or financial product and the risk assessment conducted by the financial institution. Banks may require a certain level of collateral to secure a loan, and this collateral can vary widely depending on the asset and the terms of the loan.

In decentralized finance (DeFi), collateralization ratios are often set by smart contracts and decentralized protocols. DeFi platforms use algorithms and code to determine collateralization requirements. These ratios can vary significantly from one DeFi protocol to another and are typically governed by the rules established within each protocol's smart contract. DeFi platforms often allow for greater flexibility and innovation in setting collateralization ratios, but they also come with their own unique risks and uncertainties.

Although it is described differently across various sources, collateralization is essentially the process by which a borrower pledges a pre-owned asset as assurance that the lender can recoup their capital in the event that the borrower defaults on their loan, or fails to fulfill the lending terms.

Prior to the inception of decentralized finance (DeFi), collateralization was a term commonly used in traditional finance. Aside from the banks, collateralized loans are also common in the stock and forex markets. For example, in margin trading, an investor borrows money or other valuable assets from a broker in order to buy stocks. However, to do this, the investor must set aside a sum in their brokerage account as collateral (typically either equal to, half of, or greater than the agreed-upon amount). Once this is done, the loan increases the number of shares the investor can buy, thereby multiplying their potential gains if the shares increase in value. In the same vein, this move also increases an investor’s exposure in the event that the shares don’t increase in value. In this case, a broker can retain possession of the collateral, while the borrower tries to fulfil the obligations laid out in the terms of the borrowing agreement.

History of Collateral

While collateral has been used for hundreds of years, not much has changed in terms of how it functions. However, collateral management did not begin until the 1980s, when institutions like Bankers Trust and Solomon Brothers began accepting collateral against credit exposure, at around the same time that collateralization of derivatives exposures was becoming more widespread. At its essence, collateralization involves using a valuable asset to back a loan. If the borrower defaults, the lender has the right to take and sell the asset to recover their losses. This mechanism can be likened to insurance, but it's designed to protect lenders. [2]

Collateral Factor, Collateralization Ratio, and LTV

The collateral factor is the maximum amount a user can borrow, represented in percentages, based on the total amount of assets supplied. It is also represented by the loan-to-value ratio (LTV) for various DeFi lending and borrowing protocols, as well as traditional financial institutions.

In the context of cryptocurrencies, if the Collateral Factor or LTV of USDC is 75%, and a user supplies 100 USDC (worth 75 (100 USDC * 75%) to borrow other assets.

Generally, more liquid or less volatile assets have higher collateral factors, which can change with market conditions. Different platforms and protocols have their own designated collateral factor depending on their assessment of the asset. If an asset has a 0% collateral factor, it cannot be used as collateral for borrowing other assets, though the asset itself can still be borrowed.[3]

Certain DeFi resources confuse the terms Collateral Factors, Collateralization Ratio, and Loan Value Ratio (LTV). Although the numbers can appear similar sometimes, the Collateral Factor is a metric established by the protocol to define the maximum amount the borrower can borrow against a specific asset supplied as collateral. In reality, the amount that the borrower should borrow is much lower, so that they can avoid being easily liquidated.

To calculate how much the borrower should really borrow, use the Loan to Value Ratio (LTV) spot calculation to make sure that their loan remains way below the Collateral Factor of the asset they are supplying as collateral. The higher the Collateral Factor of the asset the borrower is supplying as collateral, the better. It means there is more trust in that asset to remain stable.

On the other hand, a higher Loan to Value ratio means a riskier loan, so the borrower should stay on the lower side to avoid getting the DeFi loan liquidated. However, in defi, even loans with high Loan to Value ratios (riskier loans) are still overcollateralized, which can be seen by calculating the Collateralization Ratio.

See something wrong?

Average Rating

No ratings yet, be the first to rate!

How was your experience?

Give this wiki a quick rating to let us know!

Edited By

On June 18, 2026. 14:11 UTC

Edit summary:

Updated summary clarifying Collateralization Ratio definition