0% read

最后更新:

Maximal Extractable Value (MEV)

最大可提取价值 (MEV) 是区块链技术中的一个概念,指区块生产者——如矿工或验证者——通过操纵交易可以提取的最大利润。

这涉及在区块内战略性地包含、排除或重新排序交易,以获得超出标准区块奖励和交易费用的货币收益。

MEV 最初被称为“矿工可提取价值”,随着以太坊上去中心化金融 (DeFi) 平台的兴起,其相关性不断增强,因为复杂的智能合约为此类操纵提供了大量机会[1] [2] 。

历史或发展

随着以太坊上 DeFi 平台的出现,MEV 的概念变得尤为突出,这些平台允许通过智能合约进行复杂的金融交易。

2019 年发表的一篇具有里程碑意义的论文《Flash Boys 2.0》揭示了矿工如何为了利润重新排序交易,提高了人们对这一行为的认识。该术语最初与工作量证明 (PoW) 矿工相关,随着 2022 年合并后以太坊转向权益证明 (PoS),该术语已演变为涵盖区块链验证者。

Flashbots 等创新——一个允许在公共内存池之外进行私人 MEV 交易的平台——旨在通过减少公共竞争和 Gas 竞价大战来减轻 MEV 的一些负面影响[3]。

总的来说,MEV 是一把双刃剑,它在优化 DeFi 市场与潜在风险(如增加交易成本和网络拥堵)之间寻求平衡,而这些风险可能会损害整体区块链的安全性和公平性[2]。

背景与目的

MEV 的出现源于区块链交易处理中固有的特性。像以太坊这样的区块链网络通过去中心化节点运行,这些节点负责验证交易并将其添加到区块中。

这些节点(也称为区块生产者)对于根据所提供的费用包含哪些交易以及以何种顺序包含交易拥有巨大的裁量权。

MEV 利用了这一点,允许区块生产者偏好那些能使其收入最大化的交易,通常通过 DeFi 市场中的抢跑(front-running)或三明治交易(sandwich trading)来实现。

虽然这可能会通过增加交易成本和滑点来降低用户体验,但它也通过确保跨平台的平台价格一致,在提高金融系统效率方面发挥了作用[2]。

工作原理 / 关键属性

MEV 的机制涉及区块生产者利用其在交易排序中的角色。当用户向区块链提交交易时,交易会进入内存池(mempool)——一个待处理交易的队列。区块生产者可以扫描此内存池,寻找由任意交易排序创造的获利机会。

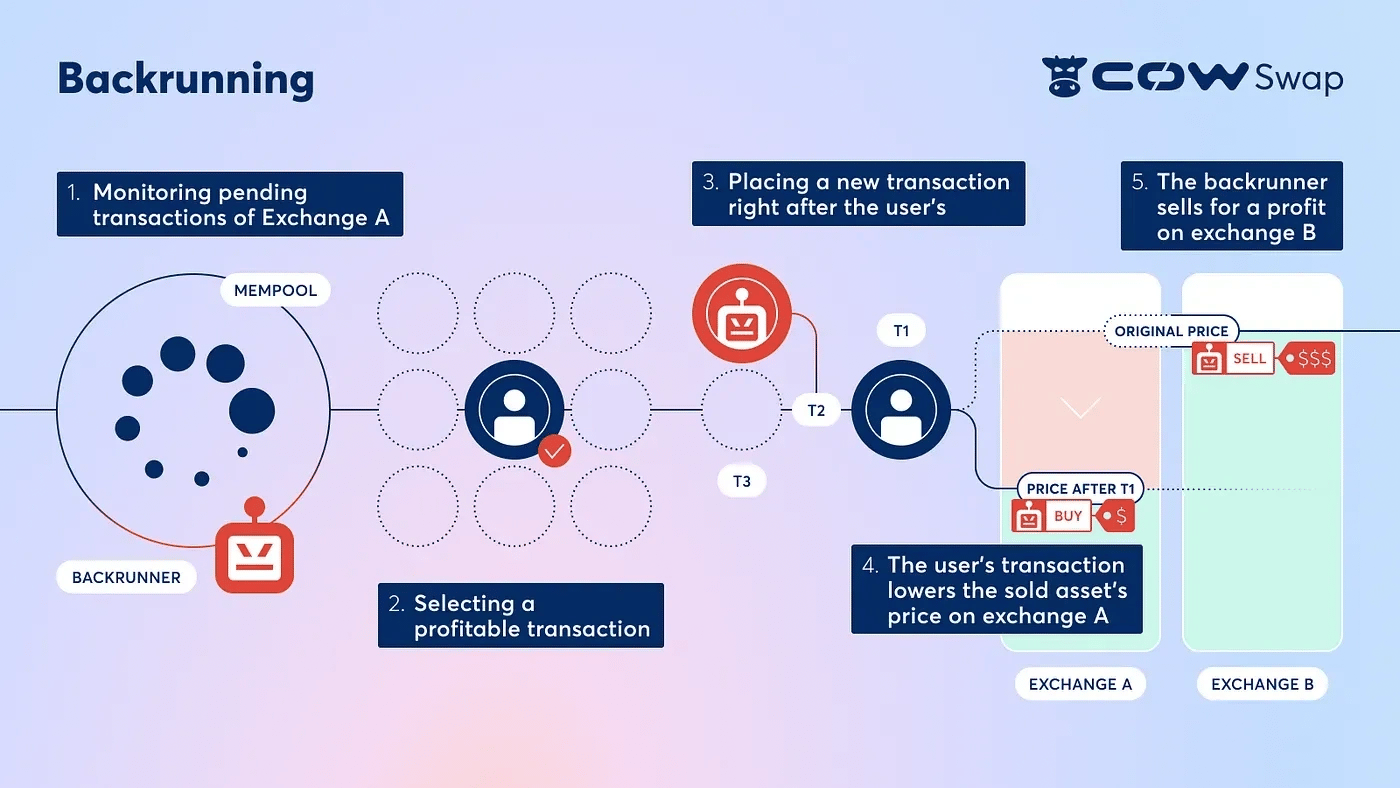

这可能意味着优先处理高费用交易以实现即时利润最大化,或者战略性地在大型交易前后放置交易以利用价格波动获利,这通常被称为三明治攻击[3]。

此外,MEV 搜索者(独立操作员)可以使用复杂的算法来识别获利的交易排序策略。这些搜索者运行机器人来检测并执行通过各种方法捕获价值的交易,例如跨去中心化交易所的套利,或在他人行动之前清算抵押贷款。

通常,这些搜索者会支付高昂的 Gas 费用,这使得验证者因优先处理其交易而获利[1]。

MEV 示例

抢跑和三明治攻击

MEV 机器人可以检测去中心化交易所内存池中的大型交易,并在这些交易之前和之后插入交易,以从价格波动中获利,导致用户遭受滑点增加的损失。

DEX 套利

去中心化交易所 (DEX) 套利是最简单且最广为人知的 MEV 机会。因此,它的竞争也最为激烈。

其工作原理如下:如果两个 DEX 以两种不同的价格提供同一种代币,有人可以在价格较低的 DEX 上购买该代币,并在单个原子交易中在价格较高的 DEX 上将其出售。得益于区块链的机制,这是真正的无风险套利。[2]

交易所套利

机器人发现同一资产在不同交易所之间的价格差异。通过在单笔交易中低买高卖,这些机器人有助于使价格正常化,但代价是牺牲了原始交易的意图。

清算

区块链借贷协议依靠搜索者来执行超额抵押贷款的及时清算。通过抢在他人之前提交清算交易,机器人可以获取费用,确保贷方获得偿付,但增加了借款人的费用[2]。

广义抢跑

机器人跟踪公共内存池,复制潜在获利的交易并将地址替换为自己的地址,如果成功则会产生潜在利润[1]。

NFT MEV

NFT 领域的 MEV 是一种新兴现象,且不一定总是获利的。[2]

然而,由于 NFT 交易发生在所有其他以太坊交易共享的同一个区块链上,搜索者也可以在 NFT 市场中使用与传统 MEV 机会类似的技术。

例如,如果有一个热门的 NFT 投放,而搜索者想要某个特定的 NFT 或一组 NFT,他们可以编写交易程序,使自己排在购买 NFT 的首位,或者在单笔交易中购买整套 NFT。或者,如果一个 NFT 被错误地以低价挂出,搜索者可以抢在其他购买者之前将其低价购入。[2] [3]

发现错误了吗?

平均评级

暂无评分

您的体验如何?

给这个维基一个快速评分让我们知道!

编辑者

2026年6月18日。14:21 UTC

编辑摘要:

Expanded MEV summary to include Ethereum DeFi context