0% read

Last updated:

Crypto Week

Crypto Week is a legislative initiative in the U.S. House of Representatives, announced for the week of July 14, 2025, aimed at advancing key legislation to establish a regulatory framework for digital assets and solidify the United States' position as a global leader in cryptocurrency innovation [1].

Overview

The initiative was announced by House Committee on Financial Services Chairman French Hill, House Committee on Agriculture Chairman GT Thompson, and House Leadership. Its primary goal is to create a clear and comprehensive regulatory environment for digital assets, focusing on consumer and investor protection, stablecoin regulation, and preventing the issuance of a U.S. Central Bank Digital Currency (CBDC). This push is part of a broader effort to make the United States the "crypto capital of the world," aligning with the agenda of the Trump Administration [1].

The concept of a dedicated "Crypto Week" emerged from years of legislative work and discussions within Congress. This included numerous hearings, roundtables, and the introduction of various bills related to digital asset market structure, payment stablecoins, and CBDCs. Key committees, including the House Financial Services Committee and the House Agriculture Committee, have collaborated extensively on these legislative efforts, seeking input from innovators, creators, and legal experts in the digital asset ecosystem [1].

Legislation to be Considered

During Crypto Week, the House of Representatives planned to consider three significant pieces of legislation:

- CLARITY Act: This bill aims to establish a clear market structure for digital assets, defining when an asset is considered a security (regulated by the Securities and Exchange Commission, SEC) versus a commodity (regulated by the Commodity Futures Trading Commission, CFTC). It seeks to provide regulatory certainty for the industry [1] [2].

- Anti-CBDC Surveillance State Act: This legislation is designed to permanently block the creation of a Central Bank Digital Currency (CBDC) in the United States, with proponents arguing it safeguards Americans' financial privacy and prevents government overreach into the digital economy [1] [2].

- GENIUS Act: This stablecoin bill, which had already passed the Senate, focuses on providing rules for the issuance and operation of dollar-backed payment stablecoins. Its passage in the House would make it the first standalone crypto measure signed into law [1] [2].

Legislative History and Milestones

The legislative groundwork for Crypto Week spans several years and includes numerous committee actions:

- February 4, 2025: A bicameral working group focused on digital asset legislation for payment stablecoins and market structure was announced by Chairmen Hill, Thompson, Scott, and Boozman, alongside President Trump’s White House A.I. and Crypto Czar, David Sacks [1].

- February 11, 2025: The Subcommittee on Digital Assets, Financial Technology, and Artificial Intelligence held a hearing titled “A Golden Age of Digital Assets: Charting a Path Forward” [1].

- March 11, 2025: The Financial Services Committee held a hearing titled “Navigating the Digital Payments Ecosystem: Examining a Federal Framework for Payment Stablecoins and the Consequences of a U.S. CBDC” [1].

- April 2, 2025: The Financial Services Committee reported the STABLE Act and the Anti-CBDC Surveillance State Act to the full House for consideration [1].

- April 9, 2025: The Subcommittee on Digital Assets, Financial Technology, and Artificial Intelligence held its first digital asset market structure hearing of the current Congress [1].

- May 5, 2025: A digital asset market structure discussion draft was released by Chairmen Hill, Thompson, Steil, and Johnson [1].

- May 6, 2025: The House Committees on Financial Services and Agriculture held a joint roundtable discussion on digital asset market structure [1].

- June 10, 2025: The CLARITY Act was reported by the Financial Services Committee (32-19) and the House Agriculture Committee (47-6) to the full House of Representatives [1].

- June 11, 2025: Chairmen Hill, Thompson, and Majority Whip Emmer published an op-ed in CoinDesk reaffirming their commitment to comprehensive digital asset legislation [1].

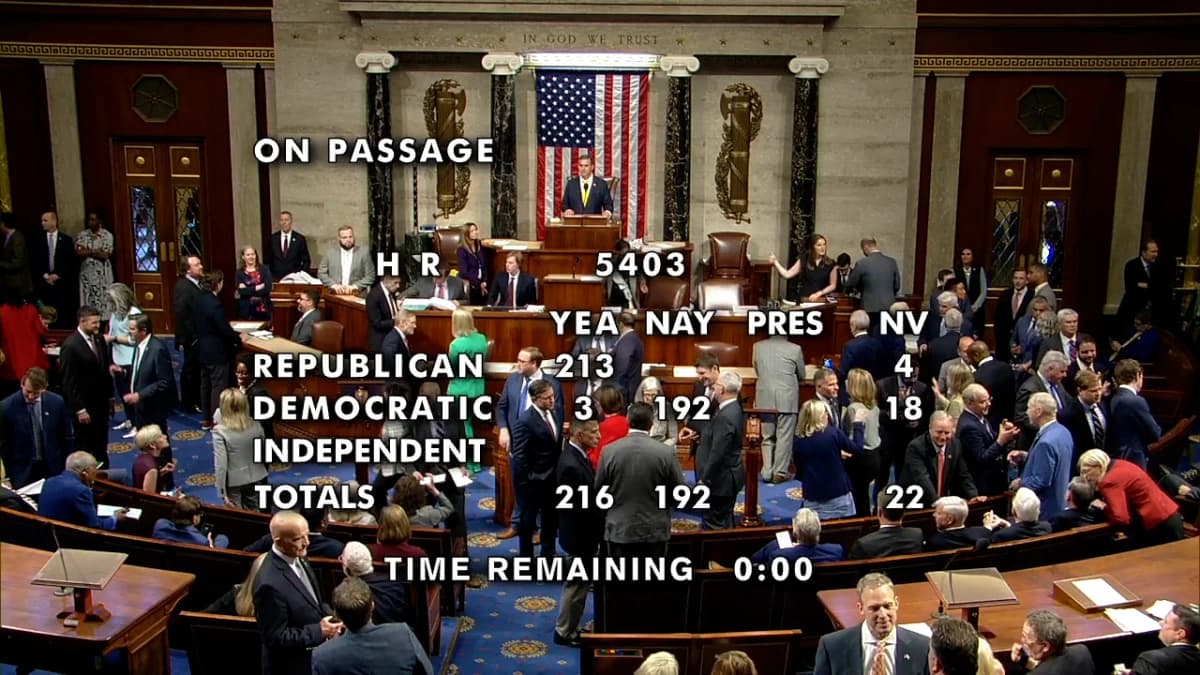

- May 22, 2024 (118th Congress): The House passed the Financial Innovation and Technology for the 21st Century Act (FIT21), the first comprehensive digital asset market structure legislation, with bipartisan support (71 Democrats, 208 Republicans). The CBDC Anti-Surveillance State Act also passed the House (216-192) [1].

Controversies and Challenges

Despite strong bipartisan support for some aspects of crypto legislation, Crypto Week faced procedural hurdles and political controversies. On July 15, 2025, a procedural vote to bring the crypto bills to the floor stalled when 13 Republicans joined all Democrats in opposition. This unexpected blockage temporarily halted the legislative process [3].

A key point of contention, particularly for Democrats, was the perceived conflict of interest related to President Donald Trump's growing involvement in the crypto industry. Concerns were raised about the Trump family's ventures, including meme coins ($TRUMP, $MELANIA), a stablecoin ($USD1), and a decentralized finance firm (World Liberty Financial). While the Senate-passed GENIUS Act includes a provision barring members of Congress and their families from profiting from stablecoins, this prohibition does not extend to the President or his family, leading to criticism from some lawmakers like Senator Raphael Warnock [2] [3].

The procedural disagreement among Republicans centered on whether the three bills should be passed individually or as a single package. Some Republicans advocated for packaging the bills, expressing skepticism about the Senate's willingness to advance the House's market structure legislation independently. President Trump, however, urged the House to pass the bills individually to expedite the stablecoin legislation to his desk before the August recess [3].

Following the initial procedural setback, President Trump intervened, holding a late-evening meeting with Republican lawmakers in the Oval Office. He successfully garnered the support of 11 of the 12 necessary Congress members to vote in favor of the procedural step, putting the bills back on track for consideration [3].

Industry and Political Reactions

The cryptocurrency industry, including major players like Coinbase and Ripple, actively lobbied for the passage of the CLARITY Act and other related bills, believing that regulatory certainty would encourage further investment and innovation in the crypto space. Coinbase, for instance, engaged in an advertising campaign that included distributing chocolate bars in Washington D.C., citing polling data indicating significant crypto ownership among Americans [2].

Industry leaders expressed both optimism and frustration regarding the legislative process. Faryar Shirzad, Chief Policy Officer of Coinbase, acknowledged the setbacks but emphasized the importance of identifying lawmakers committed to advancing pro-crypto legislation. Crypto super PACs, such as Fairshake, have amassed significant funds (over $140 million) to influence future elections and ensure the election of crypto-friendly lawmakers, signaling the industry's long-term commitment to shaping policy [3].

Senate leaders, including Senate Banking Chair Tim Scott and Senator Cynthia Lummis, are also working on their own market structure bill, which is expected to differ slightly from the House version. Senator Kirsten Gillibrand also indicated a willingness to work with Republicans on a bipartisan bill, highlighting ongoing efforts in the Senate to address digital asset regulation [2].

See something wrong?

Wiki Powered byIQ

Categories

Tags

Verification

Events

Views

4,834

Categories

Tags

Verification

Events

Views

4,834

Average Rating

Based on over 1 ratings

How was your experience?

Give this wiki a quick rating to let us know!

Edited By

On July 26, 2025. 13:36 UTC

Edit summary:

Update content ID: Replaced old hash with new for the latest resource version.