0% read

Last updated:

Particle Trade

Particle is a platform that hosts liquidity restaking protocols, facilitating permissionless leverage trading and interest rate swaps with its Leverage Automated Market Maker (LAMM). [1]

Overview

Particle’s LAMM is a permissionless protocol designed for trading ERC-20 tokens with leverage, akin to how Uniswap popularized AMMs for trading any token. It ensures liquidity providers (LPs) earn higher yields without increased impermanent loss compared to traditional AMMs like Uniswap v3. Liquidity supplied to LAMM initially supports swapping in the AMM. When borrowed for leverage trading, this liquidity continues earning yields as if still used for swapping and a position fee through liquidity restaking. Borrowed liquidity remains locked for up to 3 days before reclaiming. [2]

LAMM operates without relying on price oracles, guaranteeing LP positions are mathematically made whole with each leverage position. This eliminates risks associated with price oracle manipulation. Unlike protocols with price-based liquidation mechanisms, LAMM employs a premium model akin to fixed-term borrowing, reducing the likelihood of liquidation even during adverse price movements. Furthermore, LAMM minimizes counterparty risk by deriving profit and loss directly from the underlying asset's price movements, ensuring potential positive returns even in volatile market conditions. [2]

Features

Open Positions

Leverage trading on LAMM allows traders to go long or short on ERC-20 tokens using their paired tokens, contingent upon available liquidity. The level of leverage is constrained by the depth of liquidity for each token pair. Opening a leverage position requires payment of collateral and premium. Collateral represents the maximum potential loss if the price moves unfavorably. Premium covers interest accrual, with any excess refunded upon position closure. [3]

Each leverage position incurs three fees: an open swap fee, an open position fee, and a close swap fee. These fees compensate liquidity providers (LPs) from the underlying AMM and are deducted from the collateral, factored into the profit and loss calculation. The premium, equivalent to 2% of the collateral, is paid upfront, with interest accruing based on the swapping activities of the underlying AMM. The front end displays an hourly borrowing rate reflecting this interest accrual. Liquidation occurs when the interest accrued exceeds the premium. [3]

Close Positions

The front end provides a simulated Profit and Loss (PnL) calculation based on factors like entry price, current price, leverage ratio, accrued interest, and fees. However, the realized PnL at position closing may slightly differ due to price impacts, which are protected against slippage. [4]

Because of the mathematical nature of AMMs, accurately tracking the resulting price point after a swap can be challenging. Therefore, when a position is closed, a small residual amount of the position token might be left (e.g., WETH if the trader used USDC to long WETH). This residual is returned to the trader's wallet upon position closing. Subsequently, the trader can convert it back into the source token. [4]

Liquidation

The LAMM protocol operates on a premium model akin to fixed-term borrowing. Liquidation occurs if the interest accrued on a position exceeds the upfront premium or the position reaches the 3-day mark after liquidity reclaiming by the LP. Until these conditions are met, positions remain unaffected by adverse token price movements. [5]

Interest accrual rates align with the underlying AMM. The front end provides a liquidation page listing all liquidatable or imminent positions. Anyone can act as a liquidator for any such position, receiving a 5% reward on the position's premium. [5]

Following liquidation, the LP retrieves the borrowed liquidity and swapping fees accumulated during the borrowing period. The borrower receives the realized Profit and Loss (PnL) at the price of the liquidation event, adjusted by subtracting the liquidation reward. [5]

Duo Exchange

Duo Exchange is a yield-swapping protocol where LPs can enhance their airdrop points or yield. A central Vault contract consolidates liquidity from all LPs and directs points or yield based on each LP's chosen preferences. For each LP's deposit of native ETH, WETH, or USDB into Duo Exchange, an equivalent amount of Duo Restaking Tokens (DRTs) such as DETH or DUSD is minted. These DRTs can be utilized in various protocols, such as serving as collateral in lending platforms, currency swaps, or leverage trading activities. Upon withdrawal, LPs must ensure an equivalent amount of DRTs is available in their wallet to redeem the original principal at a 1:1 ratio. [6][7]

Point-Yield Swap

Point-Yield Swap on Duo Exchange lets LPs choose between boosted points or boosted yield. Both liquidity flows are accommodated within a single vault contract. There are two types of liquidity provision in the vault: LP1 and LP2. LP1 provides liquidity to receive boosted points while foregoing the yield, whereas LP2 provides liquidity to receive boosted yield while foregoing the points. [8]

LP1 enjoys a higher point rate because both LP1's and LP2's principals generate points specifically for LP1. Conversely, LP2 receives a higher yield rate because both LP1's and LP2's principals generate yield specifically for LP2. [8]

Variable-Fixed Yield Swap

The Variable-Fixed Yield Swap on Duo Exchange allows LPs to choose between a fixed-rate yield until maturity and a variable, potentially higher yield than the yield source. Both options are housed within a single Vault contract, accommodating both liquidity flows. [9]

- Liquidity Flow: The vault on Duo Exchange facilitates two methods of liquidity provision: LP1 and LP2. LP1 locks liquidity to earn a fixed yield rate until maturity, while LP2 opts for a variable rate, often surpassing the source rate over time. LP2 benefits from potentially higher rates because LP1 locks in at a lower, fixed rate from the source. Any excess yield earned by LP1 is directed into LP2. Moreover, opening an LP1 position incurs a position fee paid to LP2. [9]

- Fixed Rate Yield: In an environment with fluctuating yields, locking in a specific yield upfront becomes advantageous. The rate available for locking is determined by market conditions, enabling LP1 to effectively purchase an asset at a discount and gain full access to it at maturity. LP1 can exit before maturity, albeit without receiving the full yield. The vault handles Any unmatured portion, with the remaining yield distributed among all LP2s. [9]

- Variable Rate Yield: LP2 benefits from variable yields that trend higher over time than the yield source. This advantage arises because both LP1 and LP2 contribute to generating yields. LP1 locks in a smaller portion of the total yield pie (choosing a lower yield than the instantaneous estimate), leaving more yield for LP2. Additionally, LP2 earns a position fee from LP1. LP2 retains the flexibility to exit at any time and receives a yield and position fee proportionate to its principal sum relative to the total LP2 principal sum over time. [9]

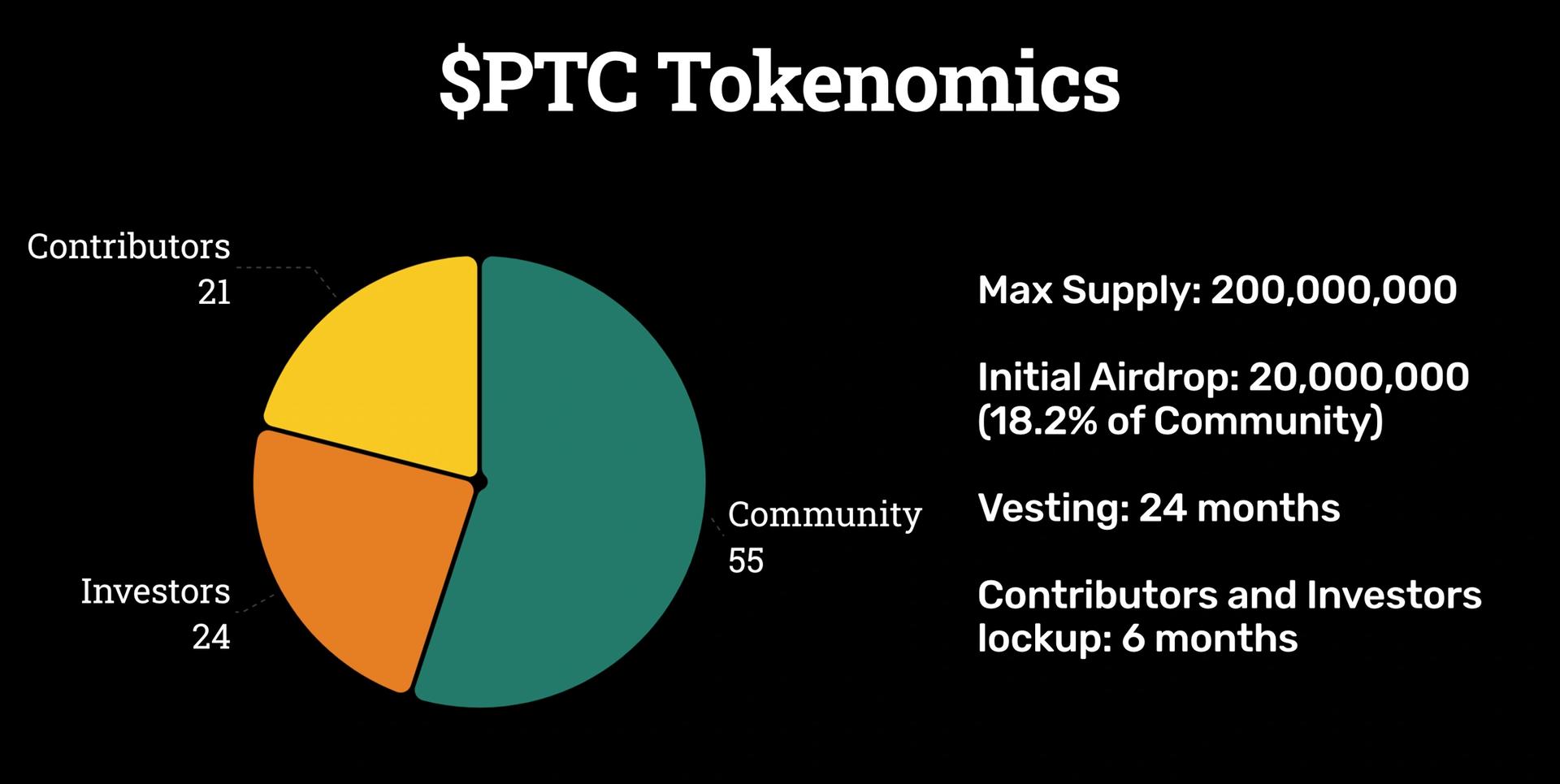

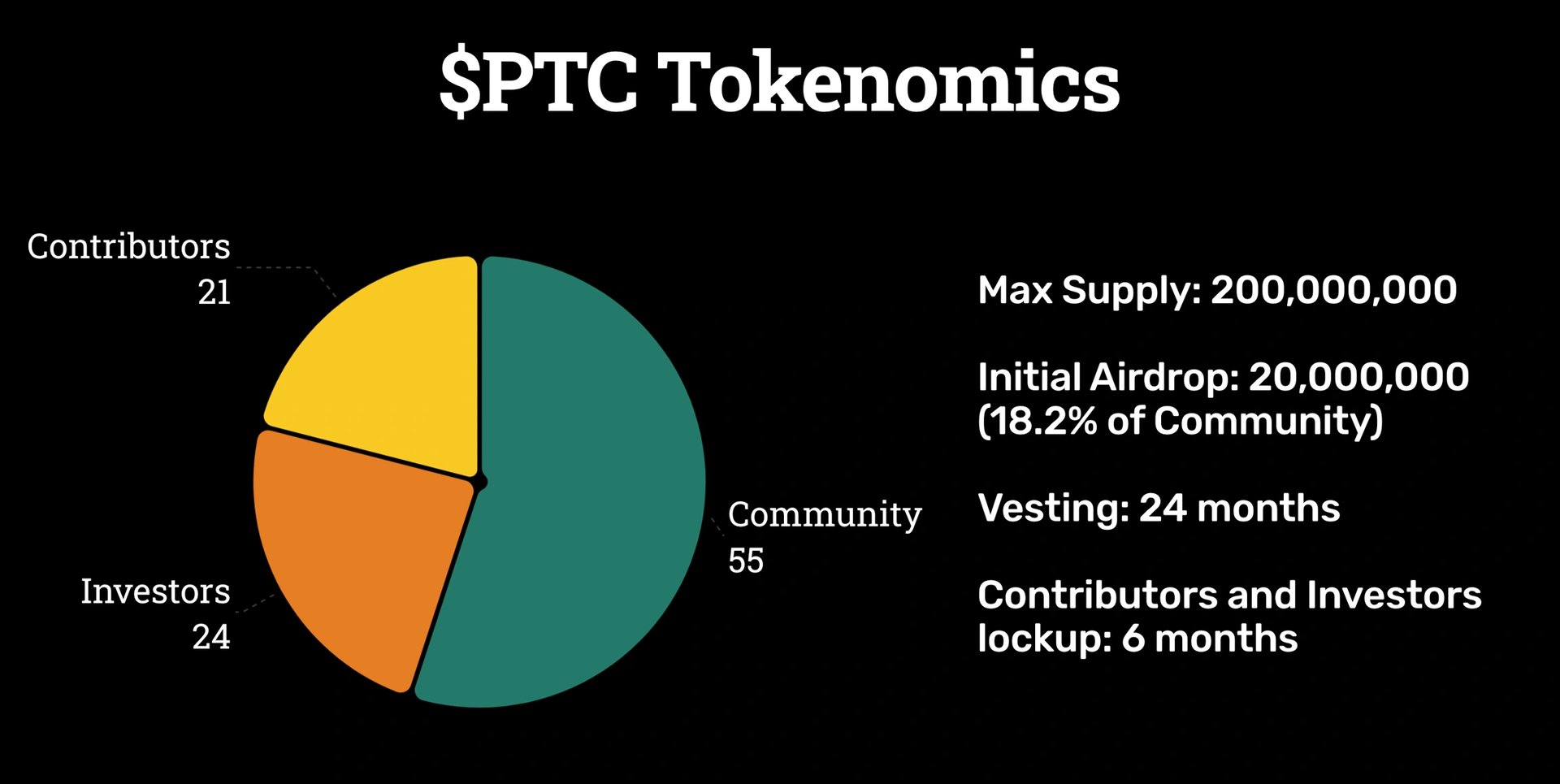

PTC Token

$PTC is the native token that governs and powers Particle's current and upcoming protocols. It has a maximum supply of 200,000,000 tokens and has the following allocation: [10]

- Community: 55%

- Investors: 24%

- Contributors: 21%

Partnerships

Investors

In January 2024, Particle raised a seed round led by Polychain Capital to facilitate permissionless leverage trading. Investors such as Nascent, Inflection, Neon DAO, Naveen Jain, Arthur Hayes, DCF God, Sam Williams, Kalos, Richard Ma, Palmer, vxCozy, and numerous other partners supported the journey. [11]

Blast

On January 17th, 2024, Particle Labs announced that Particle would be built on the Blast blockchain and participating in Blast’s Big Bang Competition to win a developer airdrop that would go to their community fund.

See something wrong?

Average Rating

Based on over 2 ratings

How was your experience?

Give this wiki a quick rating to let us know!

Edited By

On July 11, 2024. 19:41 UTC