0% read

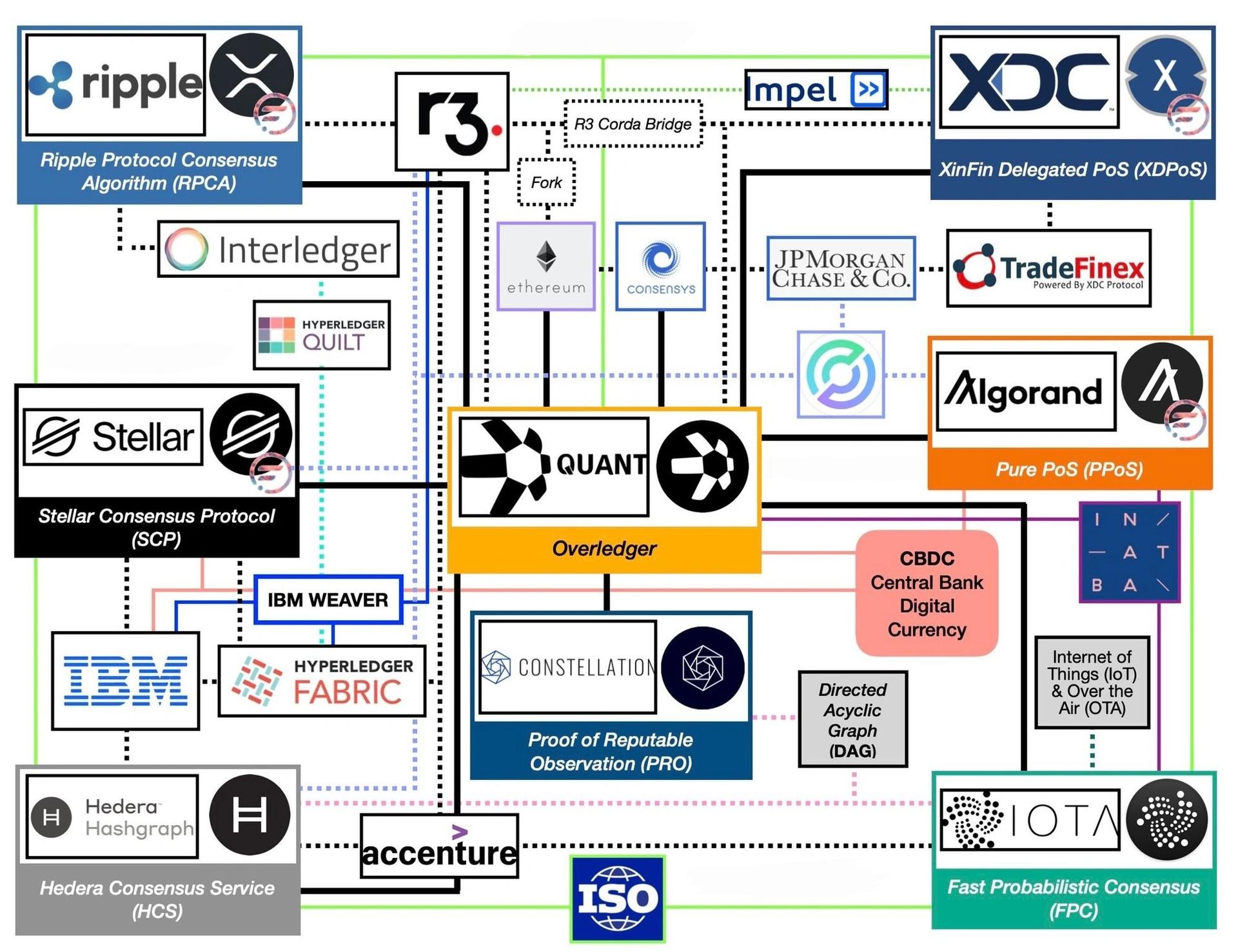

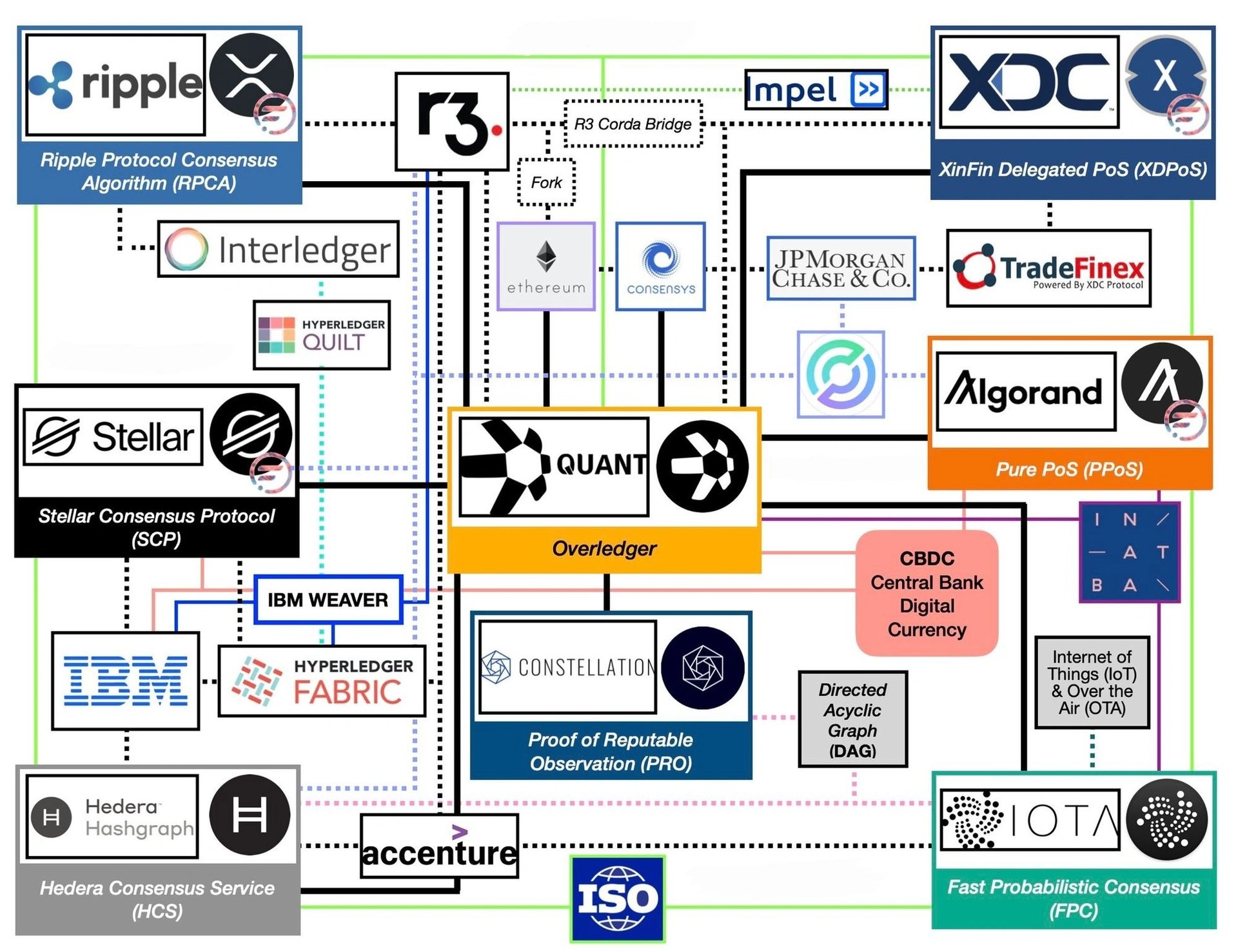

ISO 20022

ISO 20022

ISO 20022는 금융 기관 간의 금융 정보 디지털 전송을 규제하는 국제 표준입니다. 국제표준화기구(ISO)에서 개발한 ISO 20022는 금융 메시징에 대한 일관되고 적응 가능한 접근 방식을 제공하여 은행 및 금융 거래의 상호 운용성과 효율성을 향상시킵니다.[1]

개요

ISO 20022는 금융 기관 간의 전자 데이터 교환을 위한 통일된 프레임워크를 제공하는 국제 표준입니다. 원래 전통적인 금융을 위해 만들어진 ISO 20022는 현재 암호화폐 애플리케이션에서 사용되고 있습니다.

ISO 20022는 금융 통신을 표준화함으로써 암호화폐 부문의 질서와 상호 운용성을 개선하여 다양한 플랫폼과 네트워크 간의 안정적인 상호 작용을 가능하게 합니다. 이 표준은 보편적으로 인정되는 통신 언어에 대한 금융 부문의 요구를 충족합니다. 이를 통해 이러한 조직은 파트너와 상호 작용하고 글로벌 플랫폼에서 비즈니스를 수행할 수 있습니다.

ISO 20022는 다양한 부서와 조직 간의 직접적인 통신을 촉진하여 은행, 암호화폐 회사 및 중개 회사와 같은 금융 기관에 대한 애플리케이션을 제공합니다. 이를 통해 다양한 통신 네트워크 유지 비용을 절감할 수 있습니다. 또한 ISO 20022는 현재 프로토콜과 호환되어 다양한 금융 운영을 가능하게 합니다.

ISO 20022의 주요 목표는 다양한 금융 시스템에서 사용하는 다양한 메시지 형식과 프로토콜을 대체할 국제 표준을 제공하는 것입니다. ISO 20022를 구현함으로써 금융 기관은 데이터 전송의 정확성과 보안을 높이고 운영을 간소화할 수 있습니다. [1][2]

ISO 20022

UFL(Universal Financial Language)이라고도 하는 ISO 20022는 금융 통신을 위한 표준 언어 역할을 하여 금융 기관과 SWIFT와 같은 글로벌 결제 네트워크 간의 통신을 용이하게 합니다. 이 표준은 금융 거래의 효율성, 정확성 및 상호 운용성을 향상시킵니다.

ISO 20022와의 호환성:

-

전통적인 금융 기관: 은행, 중개인 및 기타 금융 기관은 고객 및 파트너와의 안전하고 원활한 통신을 보장하기 위해 2025년까지 ISO 20022를 준수해야 합니다.

-

암호화폐 회사: ISO 20022와의 통합은 은행 및 기타 금융 시스템과의 상호 운용성을 가능하게 하여 암호화폐의 더 넓은 시장 채택과 수용을 장려합니다.

-

핀테크 회사: 혁신적인 금융 서비스를 제공하는 핀테크 회사는 글로벌 금융 시스템에 통합하기 위해 ISO 20022와의 호환성을 보장해야 합니다.

진화하는 금융 환경의 새로운 비즈니스 모델은 ISO 20022와 호환되어야 합니다. 이 표준과의 통합은 새로운 금융 솔루션의 생성을 지원하고 보다 효율적이고 포괄적이며 상호 운용 가능한 금융 미래에 기여합니다. [2][3] 이러한 적응에 대한 수요 증가의 한 예는 XRP 암호화폐를 개발한 회사인 Ripple이 ISO 20022 표준 기관에 가입했다는 것입니다.

구현 옵션

-

새로운 금융 서비스 및 제품: ISO 20022와 블록체인 기술의 결합은 보다 접근하기 쉽고 빠른 국제 결제, 더 안전하고 효과적인 디지털 자산 보관 솔루션 및 새로운 금융 옵션을 포함하여 새로운 금융 서비스 및 제품의 생성을 촉진합니다.

-

금융 포용: 기존 금융 시스템에 아직 포함되지 않은 개인과 기업에 보다 접근하기 쉬운 금융 서비스를 제공함으로써 ISO 20022의 채택은 경제 성장과 금융 포용을 촉진하는 데 도움이 됩니다.

-

상호 운용 가능한 금융: 금융 통신의 글로벌 표준화를 통해 보다 통합되고 상호 운용 가능한 금융 시스템 및 플랫폼이 가능합니다.

Impel의 블록체인 API

Impel은 블록체인 기술을 활용하여 ISO 20022 표준을 준수하는 금융 메시징을 제공하는 금융 기술 회사입니다. 이 플랫폼은 즉시 결제를 위한 선택적 담보를 제공하고 은행 및 핀테크 조직을 위한 R3 Corda 플랫폼에 대한 브리지를 포함합니다.

ISO 20022 및 블록체인 기술을 기반으로 하는 Impel의 API 구현은 거래 및 데이터 전송의 효율성을 향상시키는 것을 목표로 합니다.

SWIFT의 MT 및 SEPA와 같은 기존 형식은 보다 포괄적이고 자세한 ISO 20022 범용 금융 메시징 언어로 대체되고 있습니다. 2004년에 도입된 ISO 20022는 현재 70개국 이상에서 사용되고 있으며 SWIFT가 MT를 폐기하는 2025년 11월까지 의무화될 예정입니다.

Impel의 API는 ISO 20022 데이터 설명 메시지의 733개 범주를 모두 지원하여 이전 버전과의 호환성을 제공합니다. 속도, 보안 및 확장성을 제공하며 XDC 네트워크를 기반으로 합니다. 분산 원장 기술과 지분 증명(XDPoS) 합의 방법을 사용합니다.

Fluent Finance와의 협력을 통해 US+ 스테이블코인을 XDC 네트워크에 통합하여 연합 은행 파트너 컨소시엄에서 지원하는 투명하고 즉각적인 결제 솔루션을 가능하게 합니다.

Impel은 XDC 네트워크의 메인 네트워크에 저장된 실시간 금융 메시지의 생성 및 전송에 적합한 데모를 제공하고 있습니다. 또한 파일럿 프로그램과 테스트를 위한 샌드박스를 제공합니다.

국내 및 국제 결제의 경우 Impel의 ISO 20022 API는 기업 및 금융 기관의 상호 작용을 개선하고 결제 속도를 높일 수 있는 솔루션을 제공합니다. [4][5]

2024년의 ISO 20022

ISO 20022 표준을 준수하는 최초의 암호화폐 목록은 다음과 같습니다. XRP (Ripple)

- 초점: 은행 및 금융 기관을 연결하는 네트워크인 RippleNet을 통해 글로벌 결제를 용이하게 합니다.

- 이점: 빠르고 비용 효율적인 거래, 높은 처리량(초당 1,500건의 거래), 확립된 기관 채택..

- 초점: 금융 애플리케이션을 위한 안전하고 지속 가능한 인프라를 제공합니다.

- 이점: 복잡한 스마트 계약, 성장하는 DeFi 생태계 및 Ouroboros 프로토콜을 통한 보안을 지원합니다.

Quant (QNT)

- 초점: 다양한 블록체인 네트워크와 기존 금융 시스템 간의 상호 운용성.

- 이점: 다양한 블록체인 환경 간의 통신을 가능하게 하고 상호 운용 가능한 분산 솔루션 개발을 용이하게 합니다.

- 초점: 실제 애플리케이션을 위한 확장 가능하고 안전하며 사용자 친화적인 블록체인 플랫폼을 구축합니다.

- 이점: 빠르고 저렴한 소액 결제, 고급 스마트 계약 지원, 환경 친화적인 합의 메커니즘.

- 초점: 빠르고 저렴하며 접근 가능한 국경 간 거래를 위한 글로벌 금융 네트워크를 만듭니다.

- 이점: 더 빠르고 저렴한 송금, 고유한 Stellar 합의 프로토콜, 금융 포용에 중점.

- 초점: 규정 준수 분산 애플리케이션 구축을 위한 고성능의 안전한 분산 원장 플랫폼을 제공합니다.

- 이점: 빠른 거래(초당 10,000건 이상), 보안 아키텍처 및 에너지 효율적인 합의 메커니즘.

IOTA (MIOTA)

- 초점: 특히 사물 인터넷(IoT) 생태계를 위해 설계된 안전하고 확장 가능한 거래를 가능하게 합니다.

- 이점: 수수료 없는 소액 거래, 양자 내성 암호화, IoT 내에서 데이터 및 가치 전송에 최적화된 가볍고 확장 가능한 아키텍처.

XDC Network (XDC)

- 초점: 하이브리드 블록체인 플랫폼을 통해 글로벌 무역 및 공급망 금융을 용이하게 합니다.

- 이점: 공용 및 개인 블록체인 기능 결합, 높은 거래 처리량(초당 2,000건의 거래), 규정 준수 및 효율적인 국경 간 거래.

잘못된 내용이 있나요?

평균 평점

5개의 평가를 기반으로

경험은 어땠나요?

빠른 평가를 해서 우리에게 알려주세요!

편집자

June 6, 2024. 14:22 UTC