0% read

Last updated:

Cap

Cap is a stablecoin protocol designed to provide verifiable financial guarantees through its two primary products: the dollar-denominated cUSD and the yield-bearing stcUSD. It operates as a decentralized marketplace, coordinating lending, collateral management, and yield generation through smart contracts and economic incentives involving various participant roles. [2]

Overview

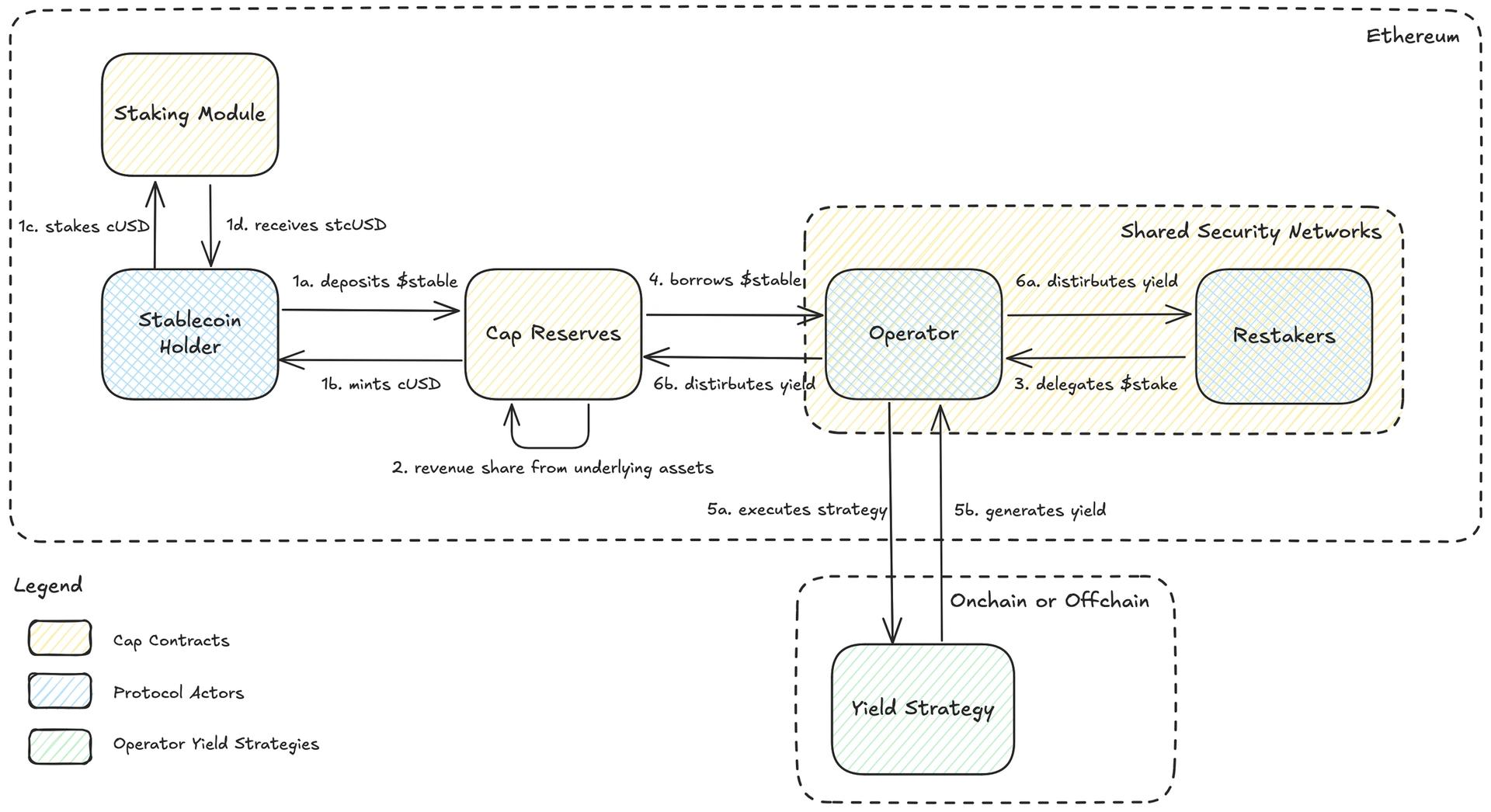

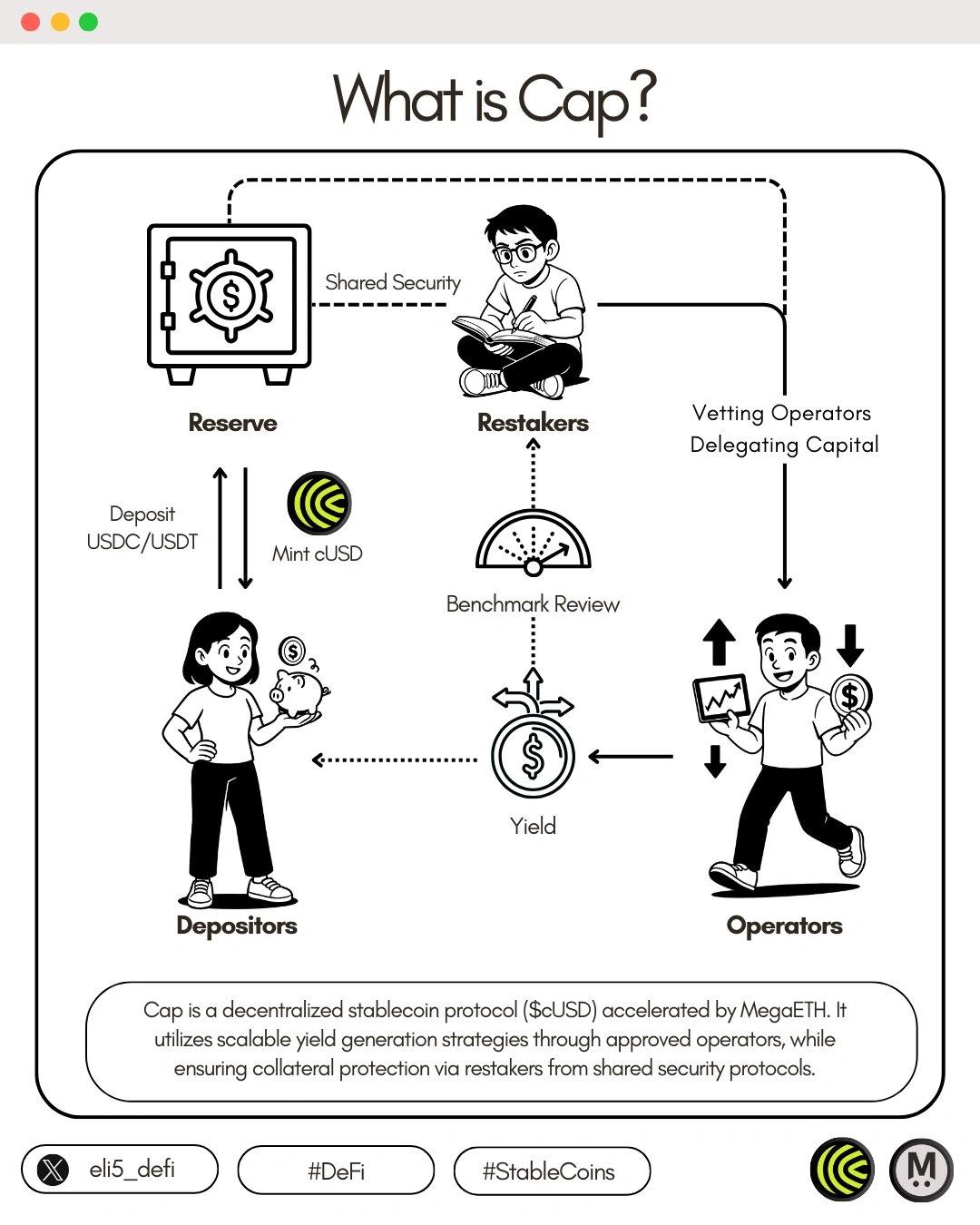

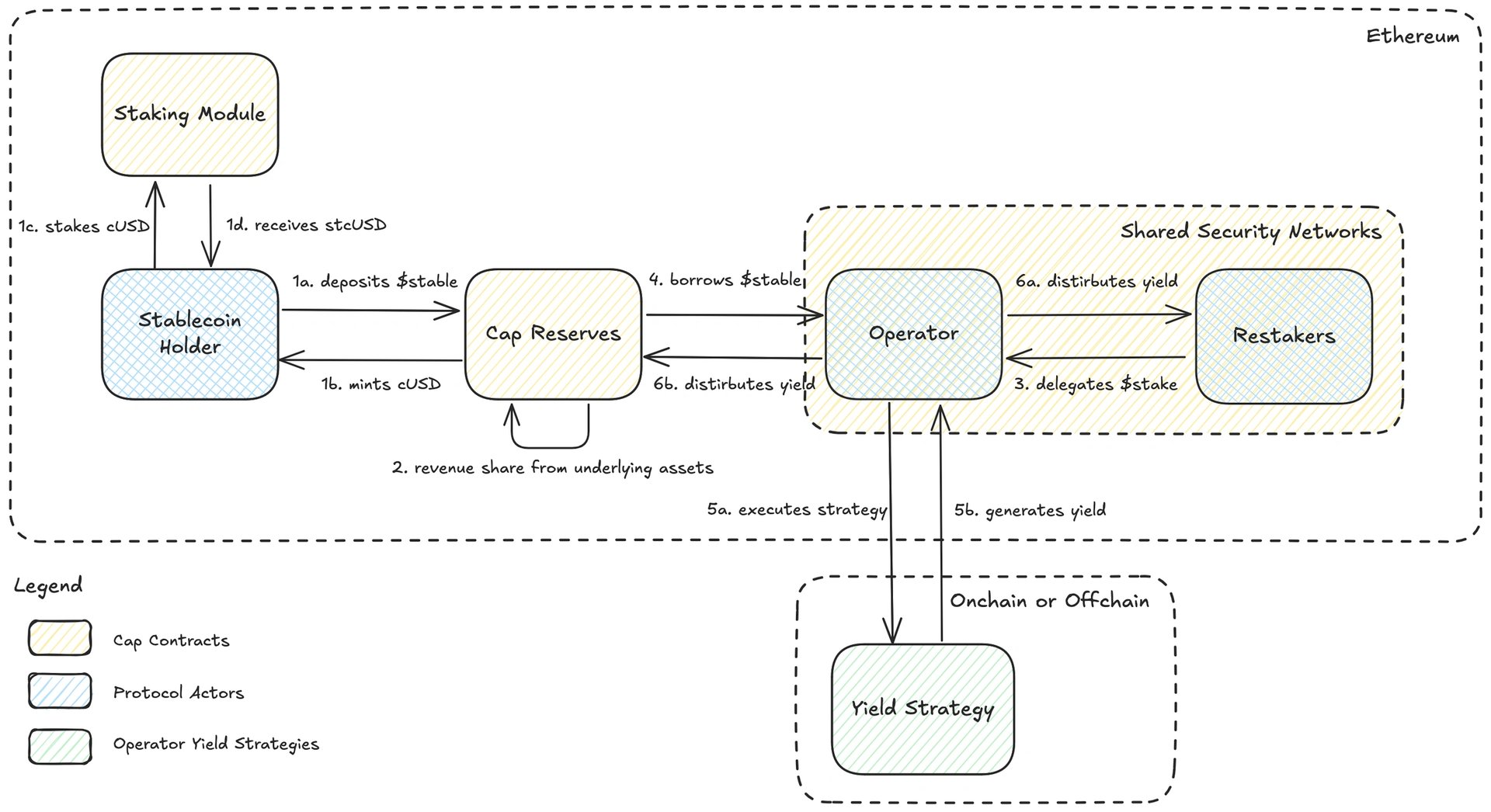

Cap is a stablecoin protocol that operates as a decentralized marketplace with three main participant groups: cUSD holders, stcUSD holders, and Operators. It issues two primary products: cUSD, a dollar-pegged stablecoin backed 1:1 by a basket of regulated, attested stablecoins such as USDC, USDT, pyUSD, BUIDL, and BENJI; and stcUSD, a yield-generating version of cUSD. Yield is generated through a network of institutional operators who borrow from the protocol to execute investment strategies, with the system designed to function autonomously through smart contracts and economic incentives.

The protocol's autonomous operation is managed by six core smart contract modules:

- Vault: Stores reserve assets, issues cUSD tokens, and provides liquidity to the Lender module.

- Lender: Handles borrowing, repayment, liquidation, and interest rate calculations.

- Fee Auction: Converts generated yield and fees into cUSD through a Dutch auction mechanism.

- Delegation: Integrates with shared security networks to manage delegated collateral, rewards, and slashing.

- Oracles: Utilizes price oracles for asset valuation and rate oracles for interest calculations.

- Access Controls: Implements granular, function-level access controls across all protocol operations.

These modules coordinate lending, collateral management, and yield generation, providing built-in downside protection and verifiable guarantees for users. [8]

Features

Type III Stablecoin

Type III stablecoins are designed to operate autonomously, utilizing smart contracts to enforce rules, allocate capital, and manage risk. Unlike models that rely on centralized teams or legal entities, Type III systems embed protections and guarantees directly into code, allowing users to verify outcomes independently. These stablecoins aim to improve safety and reduce reaction time to market changes by enabling autonomous participation in open marketplaces, where multiple yield strategies can be executed concurrently. Cap introduces the first implementation of this model, using smart contract governance and shared security mechanisms to manage third-party operator activity and enforce capital efficiency. [3]

Protocol Actors

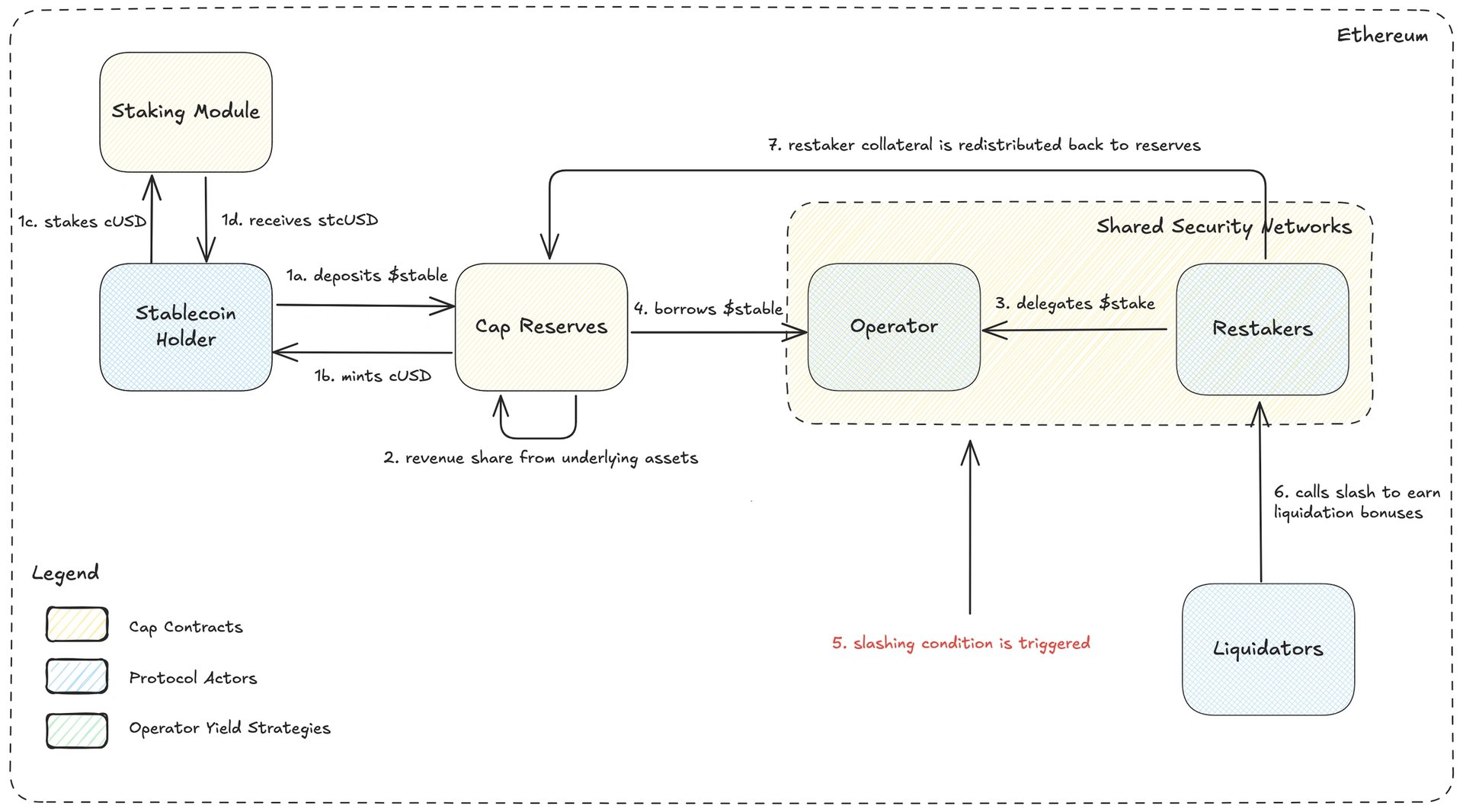

Cap's protocol involves several participant roles coordinated through on-chain rules. cUSD holders deposit approved collateral to mint cUSD, which remains fully redeemable at any time. Those who stake cUSD receive stcUSD, which earns auto-compounding yield sourced from operators executing investment strategies. Operators borrow reserve capital only if backed by delegations from restakers, who underwrite their risk.

Restakers allocate locked assets to specific operators through shared security markets and are compensated with fees. If an operator’s position becomes undercollateralized, liquidators trigger Dutch auctions to recover funds, earning bonuses for executing the auctions more quickly.

Each actor's incentives are structured: cUSD holders benefit from transparency and easy redemption; stcUSD holders receive yield with principal protection; operators can profit from surplus yield and negotiate terms with restakers; restakers set their risk premiums and receive payments in stable assets; liquidators are rewarded for efficient risk mitigation. [4]

cUSD

cUSD is a dollar-pegged stablecoin backed by a reserve of approved assets. It can be accessed through three main functions: minting (by depositing reserve assets at oracle value), burning (to redeem at the highest price deviation), and redeeming (across multiple assets to maintain peg stability). During the initial phase, certain mechanisms, such as dynamic fees and multi-collateral redemption, are inactive, and mint/burn fees are fixed at 0.25% to mitigate oracle-related risks. If oracle data is outdated, minting and burning are temporarily halted.

Unutilized collateral is placed into a Fractional Reserve, where it can generate passive yield through underlying rewards or by being deposited into integrated lending platforms, such as Aave and Morpho. Each reserve asset earns yield in ERC-4626 vaults, with allocations determined automatically based on existing revenue-sharing agreements and current interest rates. [5]

stcUSD

stcUSD is a yield-generating stablecoin built on a decentralized lending structure. Users mint cUSD by depositing approved collateral and then stake it to receive stcUSD, which accrues yield. This yield comes from two sources: rewards on idle assets and lending to operators who execute yield strategies.

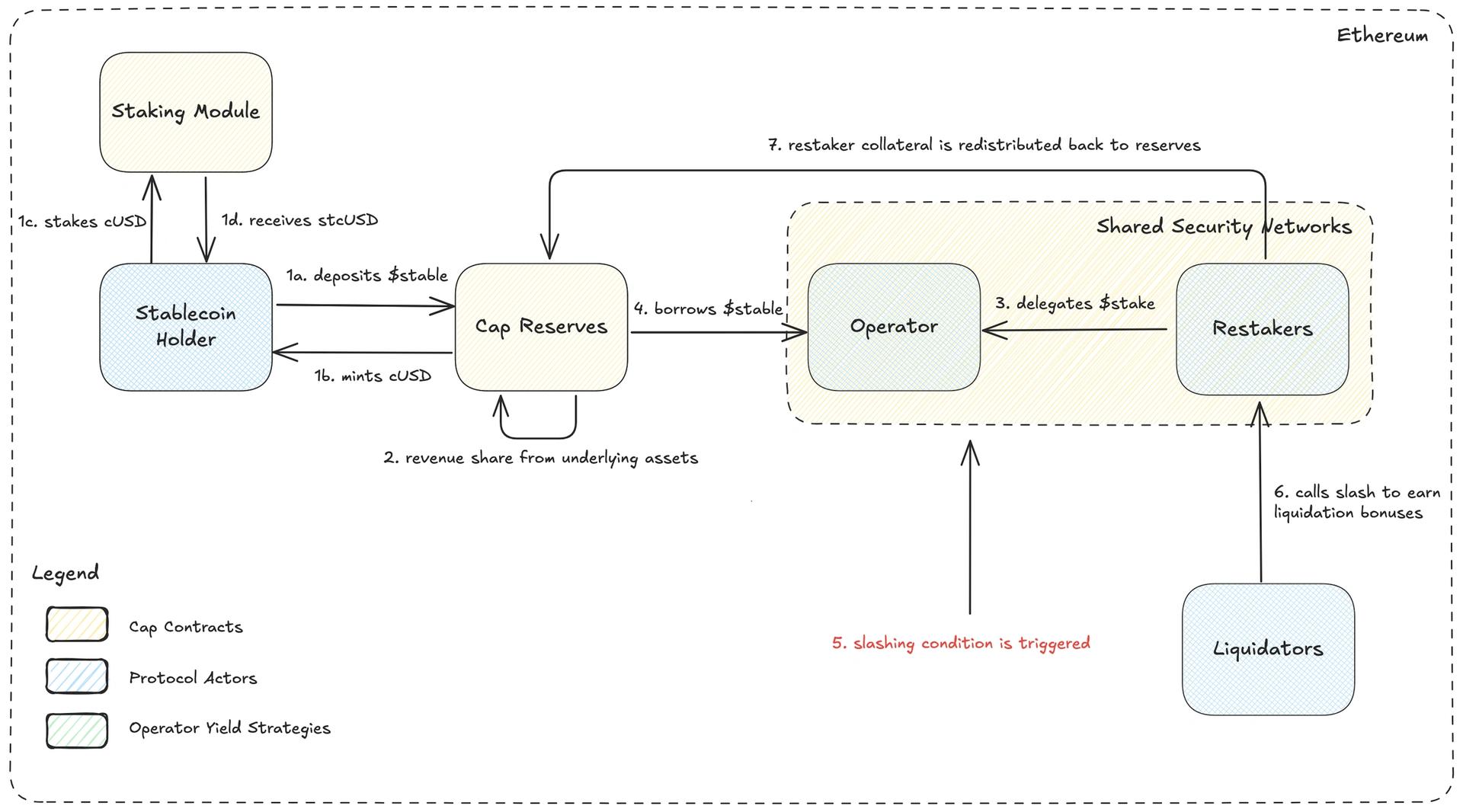

Operators must secure overcollateralized delegations from restakers to qualify for borrowing. If the operator's loan health factor drops below 1, liquidators can reduce the restaker’s collateral to cover potential losses and protect stcUSD holders. Restakers assess the operator's risk and may negotiate terms, such as loan duration and compensation. Yield is distributed to all participants when strategies perform as expected, and idle funds in the reserve are automatically deployed to integrated protocols, such as Aave or Morpho, based on current returns.

Once borrowing occurs, there are two possible paths the flow can go from here: the Happy Path or the Unhappy Path. [6]

Happy Path

In the Happy Path scenario, where the operator's strategy is successful, the loan is repaid, and the collateral remains stable, the yield is distributed among all participants. The operator executes a yield-generating strategy and repays the borrowed funds along with interest. For example, suppose a 15% return is achieved, 8% (the protocol’s hurdle rate) goes to stcUSD holders. In that case, 2% is paid to restakers as a negotiated risk premium, and the operator retains the remaining 5% as profit. [6]

Unhappy Path

In the Unhappy Path scenario—where an operator defaults or the value of their collateral drops below safety thresholds—Cap’s slashing mechanism is triggered to protect stcUSD holders. A Dutch auction is initiated to recover the operator’s outstanding debt. Liquidators step in to slash the restaker’s delegated collateral, selling it at a discount in exchange for stable assets. The recovered stablecoins are then returned to the protocol’s reserve to cover the shortfall, ensuring stcUSD holders remain protected from losses tied to failed yield strategies. [6]

Partnerships

- Triton Capital

- IMC

- Flow Traders

- SCB Limited

- Laser Digital

- GSR

- Franklin Templeton

- Symbiotic

- EigenLayer

- SatLayer

- ChainLink

Funding

Cap raised $11 million in a funding round that was announced on April 7, 2025. The round was led by Blockchain Capital, with additional participation from notable investors including a16z crypto, Dragonfly, and Lightspeed Faction. This funding aims to support the ongoing development of Cap's stablecoin protocol. [7] [8]

See something wrong?

Average Rating

No ratings yet, be the first to rate!

How was your experience?

Give this wiki a quick rating to let us know!

Edited By

On July 16, 2026. 17:03 UTC

Edit summary:

Added new wiki page Cap