0% read

마지막 업데이트:

US Treasury-Backed Stablecoins

미국 국채 담보 스테이블코인은 미국 국채 및 기타 고품질 유동 자산으로 주로 담보화되어 일반적으로 미국 달러에 1:1로 고정된 안정적인 가치를 유지하도록 설계된 암호화폐의 한 유형입니다. 이러한 디지털 자산은 기존 금융 시스템과 디지털 자산 경제 간의 주요 다리 역할을 하며 다양한 블록체인 네트워크에서 안정적인 교환 매개체, 가치 저장 수단 및 결제 자산 역할을 합니다. 그 안정성은 무담보 알고리즘 스테이블코인과 구별되는 저위험 달러 표시 자산으로 구성된 준비금을 보유함으로써 파생됩니다. [1] [2]

암호화폐 비교

US Treasury-Backed Stablecoins과(와) 가격 및 기타 지표를 비교할 자산을 선택하세요.

생태계 맵

US Treasury-Backed Stablecoins이(가) 연결된 위키와 그 관계를 맵에서 살펴보세요.

메커니즘 및 준비금 구성

미국 국채 담보 스테이블코인은 완전 준비금 모델을 통해 미국 달러에 대한 페그를 유지합니다. 발행되는 모든 스테이블코인 토큰에 대해 발행자는 지정된 분리된 준비금 펀드에 최소 1달러 상당의 자산을 보유합니다. [1] [3]

일반적인 운영 흐름은 사용자가 스테이블코인 발행자에게 미국 달러를 예치하는 것을 포함합니다. 그러면 발행자는 해당 금액의 스테이블코인 토큰을 발행하고 동시에 예치된 자금을 사용하여 승인된 준비금 자산을 구매합니다. 상환의 경우 보유자는 스테이블코인을 발행자에게 반환하고 발행자는 토큰을 "소각"하거나 파기하고 준비금에서 해당 미국 달러 가치를 반환합니다. [3]

규제 지침 및 발행자 보고서를 기반으로 준비금은 금리 위험을 완화하고 상환 요청을 충족할 수 있는 유동성을 보장하기 위해 단기, 저위험 자산에 집중됩니다. 일반적인 준비금 자산은 다음과 같습니다.

- 미국 국채 (T-bills): 단기 정부 부채 증권으로, 종종 만기가 90일 이하입니다. 이것은 가장 일반적인 준비금 자산입니다.

- 역환매 조건부 채권 (Repos): 미국 국채로 담보된 익일 계약으로, 단기 유동성을 제공합니다.

- 현금 및 현금 등가물: 보험에 가입된 예금 기관의 미국 달러 요구불 예금 계좌에 보관된 자금입니다.

- 정부 머니 마켓 펀드 (MMFs): 앞서 언급한 국채 및 환매 조건부 계약에 투자하는 펀드의 지분입니다. [1] [3]

2024년 말과 2025년 초 현재 주요 발행사의 준비금 구성은 이러한 보수적인 접근 방식을 강조했습니다. 예를 들어, Tether (USDT)는 준비금의 약 65.7%를 미국 국채에 보유하고 있으며, PayPal의 PYUSD 준비금은 95.8%의 역환매 조건부 채권과 4.2%의 현금으로 구성되어 있습니다. Circle의 USDC 준비금은 주로 국채, 현금 및 환매 조건부 거래에 투자하는 전용 펀드에 보관됩니다. [[1]](#cite-id-mTemQYtULERaxf1m]

시장 개요 및 주요 업체

미국 국채 담보 스테이블코인 시장은 기관 채택과 탈중앙화 금융(DeFi)에서의 사용 사례 확대로 인해 상당한 성장을 경험했습니다. 2024년 10월 기준으로 모든 암호화폐 거래의 80% 이상이 스테이블코인을 거래의 한 축으로 포함하는 것으로 추정되었습니다. [2]

주요 시장 데이터는 다음과 같습니다.

- 총 시가총액: 2025년 4월 현재 전체 스테이블코인 시장의 시가총액은 약 2,340억 달러입니다. [1]

- 국채 보유량: 스테이블코인 발행사들은 2024년 10월 기준으로 1,200억 달러 이상의 미국 국채를 보유하고 있는 것으로 추정되며, 이는 미국 정부 부채의 중요한 투자자 계층을 형성합니다. [2]

- 성장 전망: 재무부 차입 자문 위원회(TBAC)에서 인용한 2025년 스탠다드차타드 보고서에 따르면 규제 명확성이 확립된다는 가정 하에 스테이블코인 시장이 2028년까지 약 2조 달러의 시가총액에 도달할 수 있다고 예측했습니다. [1]

주요 발행사 및 스테이블코인은 다음과 같습니다.

- 테더(USDT): 2025년 4월 현재 시가총액이 1,450억 달러인 가장 큰 스테이블코인입니다.

- 서클(USDC): 2025년 4월 현재 시가총액이 602억 달러인 주요 규제 스테이블코인으로, 기관에서 널리 사용됩니다.

- 페이팔(PYUSD): 주요 전통 결제 회사에서 발행한 스테이블코인으로, 주류 채택이 증가하고 있음을 나타냅니다.

- 퍼스트 디지털 USD(FDUSD): 홍콩에 본사를 둔 First Digital Trust에서 2023년에 출시한 법정화폐 담보 스테이블코인으로, 현금과 미국 국채로 뒷받침됩니다. [7]

- 프랙스 USD(frxUSD): Frax Finance의 스테이블코인으로, 하이브리드 부분-알고리즘 모델로 시작했지만 이후 알고리즘 의존도를 줄이기 위해 담보 메커니즘을 변경했습니다. [8]

- 팍스 달러(USDP) 및 제미니 달러(GUSD): 투명한 준비금 관리로 알려진 NYDFS에서 규제하는 초기 스테이블코인입니다. [3]

이러한 기존 업체 외에도 새로운 프로젝트가 계속해서 시장에 진입하고 있습니다. "미국 국채 담보 스테이블코인"에 대한 CoinGecko 카테고리는 더 좁은 범위의 프로젝트를 추적하며, 그 중 일부는 Ondo US Dollar Yield (USDY)와 같이 수익을 창출합니다. 이 카테고리의 총 시가총액은 2026년 1월 기준으로 약 8억 달러였습니다. [4]

역할 및 경제적 영향

사용 사례 및 채택

재무부 지원 스테이블코인의 채택은 유용성에 의해 주도됩니다. 암호화폐 시장에서 유동성의 중요한 원천, DeFi 프로토콜의 주요 담보 형태, 변동성이 큰 포지션으로 이동하는 트레이더를 위한 안정적인 자산 역할을 합니다. [2]

암호화폐 외에도 국경 간 결제에 점점 더 많이 사용되어 기존 송금 시스템보다 빠르고 저렴한 대안을 제공합니다. 또한 신흥 시장에서 재정적 헤지 도구로 기능하여 개인이 현지 통화 평가 절하 및 높은 인플레이션으로부터 저축을 보호할 수 있습니다. 미국 달러에 고정되어 있지만 스테이블코인 사용은 주로 국제적이며, 2025년 연구에 따르면 거래의 80% 이상이 미국 외부에서 발생합니다. [5]

미국 재무부 시장과의 상호 작용

스테이블코인의 성장은 단기 미국 정부 부채에 대한 새로운 중요 구조적 수요처를 창출했습니다. 스테이블코인 공급 증가는 주로 T-Bill과 같은 준비 자산 구매 증가로 직접적으로 이어집니다. 이러한 수요는 발행자와 규제 기관이 위험을 최소화하기 위해 단기 자산을 선호하므로 수익률 곡선의 앞부분에 집중되어 있습니다. [1]

미국 재무부는 이러한 역학 관계를 인지하고 있습니다. TBAC는 2024년 10월에 재무부 발행이 증가하는 수요를 충족하기 위해 "한계적으로 T-Bill의 더 높은 비율로 기울어져야 한다"고 언급했습니다. TBAC 분석에서는 T-Bill에 대한 추가 수요가 9천억 달러에 달할 것으로 예상했습니다. [2] [1]

전통 금융에 미치는 영향

재무부 지원 스테이블코인은 전통 금융 부문에 경쟁적인 힘과 기회를 동시에 제공합니다. 무이자로 기능성이 뛰어난 결제 수단으로서 전통적인 은행 계좌에서 거래 예금을 유치할 수 있습니다. 또한 토큰화된 머니 마켓 펀드(예: BlackRock의 BUIDL)와의 융합이 증가하고 있으며, 이는 온체인 수익률을 제공합니다. 스테이블코인은 결제에 최적화되어 있지만, 토큰화된 MMF는 저위험 수익 창출 투자 역할을 하여 둘 사이에 역동적인 관계를 형성합니다. [1]

거시 경제적 수준에서 USD 페깅 스테이블코인은 미국 달러의 도달 범위와 유용성을 글로벌 디지털 경제로 확장합니다. 전 세계 개인과 기업이 달러 표시 자산에 액세스, 보유 및 거래할 수 있는 마찰 없는 방법을 제공하여 달러의 세계 주요 준비 통화로서의 위상을 강화할 수 있습니다. [1]

규제 환경

규제는 스테이블코인의 미래를 형성하는 중요한 요소이며, 위험을 해결하고 명확성을 제공하기 위해 주, 연방 및 국제적 수준에서 프레임워크가 등장하고 있습니다.

주 차원의 규제: 뉴욕 DFS

뉴욕 금융 서비스국(NYDFS)은 2022년 6월 8일에 발표된 지침을 통해 최초의 포괄적인 규제 프레임워크 중 하나를 구축했습니다. 규제 대상 발행자를 위한 주요 요구 사항은 다음과 같습니다.

- 1:1 완전 담보: 준비 자산의 시장 가치는 발행된 스테이블 코인 가치의 최소 100%여야 합니다.

- 허용 가능한 준비금: 준비금은 분리되어야 하며 미국 재무부 단기 증권(만기 3개월 이하), 특정 역레포, 미국 인가 기관의 예금과 같은 저위험 자산으로 구성되어야 합니다.

- 상환 가능성: 발행자는 보유자에게 스테이블 코인을 액면가로 즉시 미국 달러로 상환할 수 있는 권리를 부여해야 합니다.

- 월별 증명: 준비금은 독립적인 공인 회계사(CPA)가 매월 감사해야 하며 보고서는 공개되어야 합니다. [3]

연방 법률 (미국)

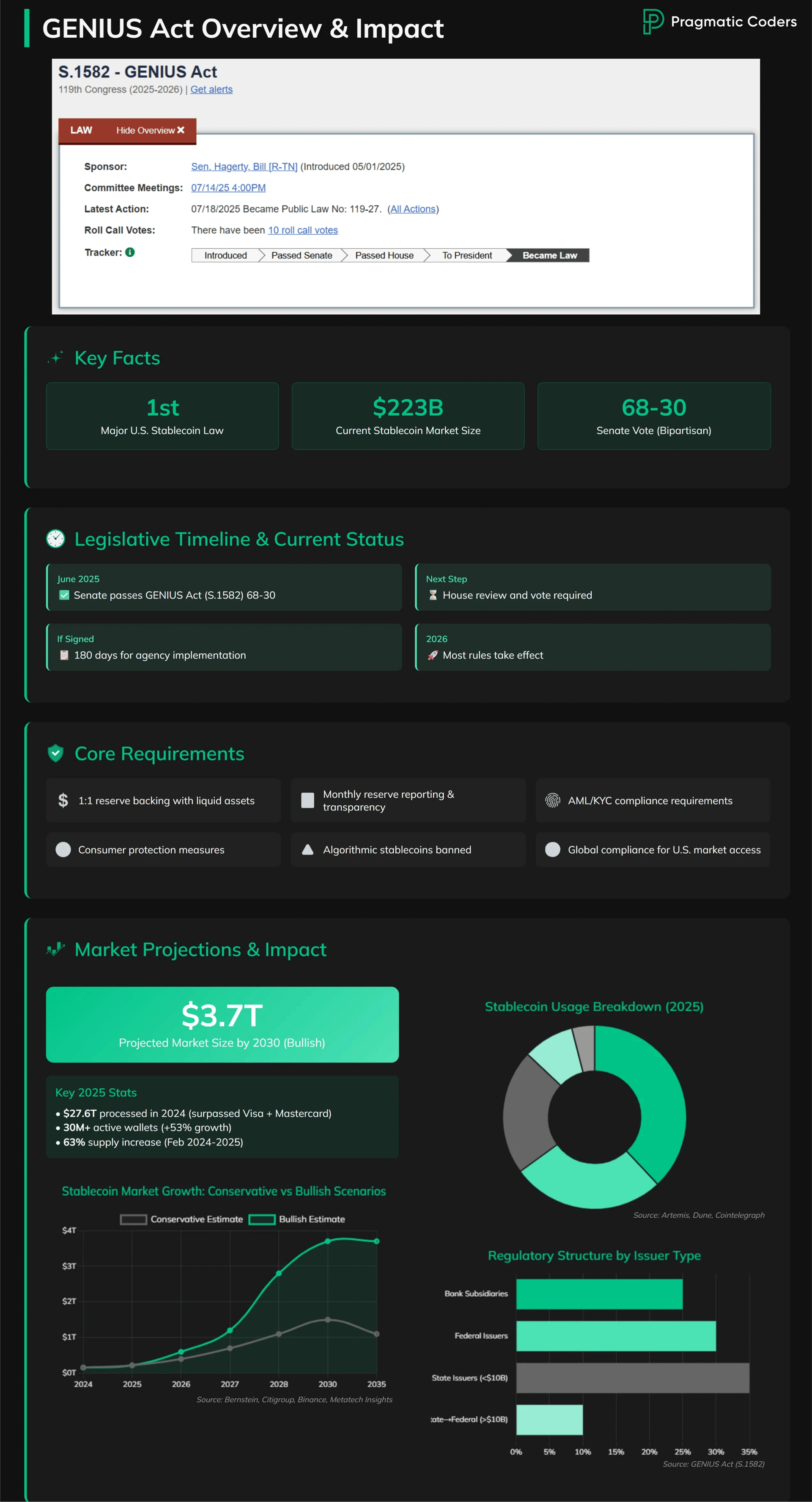

미국에서는 2025년에 [보장 및 테더 안정 경제 및 증권 통일성(GENIUS) 법(https://iq.wiki/wiki/genius-act)이 제정되어 "지불 스테이블코인"에 대한 포괄적인 연방 프레임워크를 구축했습니다. 이 법의 주요 조항은 발행자가 현금 및 만기 93일 이하의 미국 국채와 같은 고품질 유동 자산으로 1:1 지원을 유지하도록 요구합니다. 은행과 라이선스를 받은 비은행 기관 모두 스테이블코인을 발행할 수 있으며, 월별 준비 자산 공개, 공공 블록체인에서의 발행, 이자 지급 금지를 의무화합니다. [1]

또 다른 중요한 법률 노력은 2024년에 하원을 통과한 21세기 금융 혁신 및 기술 법(FIT21)이었습니다. [2]

국제 규제

유럽연합은 2024년에 암호자산 시장(MiCA) 규정을 시행하여 스테이블코인 발행, 준비금 관리 및 소비자 보호에 대한 명확한 규칙을 포함하여 암호자산에 대한 최초의 포괄적인 법적 프레임워크 중 하나를 만들었습니다. [2]

주목할 만한 프로젝트 및 개발

Citrea USD (ctUSD)

2026년 1월 15일, 금융 결제 인프라 제공업체인 MoonPay는 영지식(ZK) 증명을 활용하는 비트코인 레이어 2 네트워크인 Citrea에서 기본적으로 발행되는 미국 달러 연동 스테이블 코인인 Citrea USD(ctUSD)의 출시를 발표했습니다. 이 스테이블 코인은 단기 미국 국채와 현금으로 1:1로 뒷받침됩니다. [6]

이 프로젝트는 성장하는 비트코인 DeFi 생태계를 위한 기본 유동성 표준을 만드는 것을 목표로 합니다. Citrea 개발사인 Chainway Labs의 공동 창립자인 Orkun Mahir Kilic는 이 기본 발행 모델이 다른 블록체인의 브리지 자산으로 인해 발생하는 유동성 파편화를 해결하도록 설계되었다고 밝혔습니다. 그는 "파편화는 브리징의 증상이며, ctUSD는 Citrea에서 기본적으로 발행되므로 설계상으로 이를 해결합니다. 유동성을 분열시킬 브리지 버전이 없으며, 단 하나의 정식 자산만 있습니다."라고 말했습니다. [6]

규제 환경에 대해 Kilic는 워싱턴 D.C.의 접근 방식 변화에 대해서도 언급했습니다. "워싱턴의 이야기는 '금지'에서 '규제'로 바뀌고 있으며, 암호화폐 생태계에 진입하는 기관은 궁극적으로 상대방의 모호성을 제거하는 자산을 찾고 있습니다." [6]

Ondo US Dollar Yield (USDY)

Ondo Finance의 Ondo US Dollar Yield (USDY)는 단기 미국 국채 및 은행 요구불 예금 포트폴리오로 담보된 토큰화된 채권입니다. 1:1로 고정된 기존 스테이블 코인과 달리 USDY는 시간이 지남에 따라 가치를 축적하도록 설계된 수익 창출 자산입니다. 2026년 1월 현재 시가 총액이 6억 7,800만 달러가 넘는 CoinGecko의 "미국 국채 지원 스테이블 코인" 범주에서 가장 큰 프로젝트였습니다. [4]

OpenEden OpenDollar (USDO)

OpenEden OpenDollar (USDO)는 토큰화된 미국 국채를 담보로 OpenEden에서 발행하는 스테이블 코인입니다. 이는 수익 창출 자산으로 설계되어 보유자가 기초 T-bill에서 수익을 얻을 수 있도록 합니다. 2026년 1월 현재 시가 총액은 약 7,500만 달러입니다. [4]

Noble Dollar (USDN)

Noble Dollar (USDN)은 스테이블코인으로, Cosmos 생태계 내에서 자산 발행을 위해 설계된 애플리케이션 특정 체인인 Noble 블록체인에서 기본적으로 발행됩니다. 이 기본 발행 모델은 IBC(Inter-Blockchain Communication) 네트워크 전반에 걸쳐 사용을 용이하게 합니다. 2026년 1월 현재 시가총액은 약 3,800만 달러였습니다. [4]

Solayer USD (sUSD)

Solayer USD (sUSD)는 Solayer 프로젝트에서 발행하는 미국 국채 담보 스테이블 코인입니다. 이 범주의 다른 자산과 마찬가지로 이자를 지급하는 것으로 보이며, 시장 가격은 570만 달러 이상으로 거래되고 있습니다. [4]

MANTRA USD (MANTRAUSD)

2026년 1월 초, MANTRA 프로젝트는 MANTRA EVM 체인에서 토큰화된 실물 자산(RWA)을 위한 생태계와 관련된 스테이블 코인인 MANTRA USD(MANTRAUSD)를 출시했습니다. 이 프로젝트는 RWA 중심 플랫폼을 위한 안정적인 자산을 제공하는 것을 목표로 합니다. [4]

잘못된 내용이 있나요?

평균 평점

아직 평가가 없습니다

경험은 어땠나요?

빠른 평가를 해서 우리에게 알려주세요!

편집자

January 17, 2026. 00:35 UTC

편집 요약:

Updated content