0% read

Frax Finance

Frax Finance

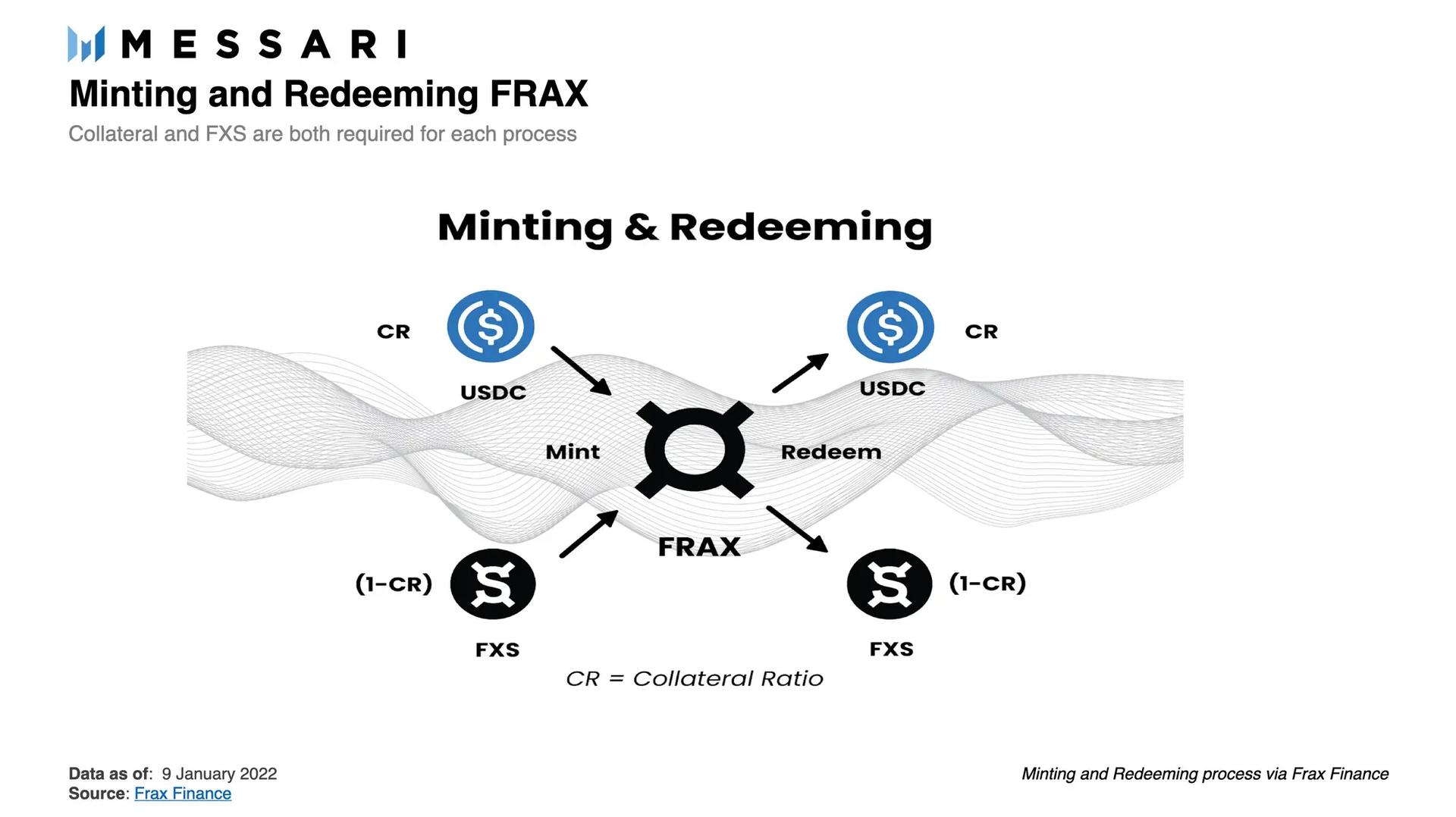

The Frax Finance Stablecoin Protocol, also known as Frax, is a stablecoin protocol that issues decentralized stablecoins and contains subprotocols to support them. Frax issues several key assets: frxUSD, a USD pegged stablecoin (formerly the FRAX stablecoin); the Frax Price Index (FPI) stablecoin, the first stablecoin pegged to a basket of real-world consumer goods; and FraxEther (frxETH), a liquid staking derivative token loosely pegged to ETH. Its liquid staking counterpart, sfrxETH, is an ERC-4626 vault token that accrues staking rewards. The ecosystem's central utility and governance token is[FRAX (formerly Frax Share or FXS), which serves as the gas token on the Fraxtal chain. The Frax Protocol also has multiple integrated subprotocols, including Fraxswap, Fraxlend, Borrow AMM (BAMM), Algorithmic Market Operations (AMOs), Fraxferry, and financial instruments like Frax Bonds (FXB) and Staked Frax USD (sfrxUSD). [30][22] [24]

The project began as "the world's first fractional stablecoin with parts of its supply collateralized and parts fractionally stabilized." [1][2] On February 23rd, 2023, the Frax Finance community voted to fully collateralize the protocol's native stablecoin FRAX.[28]

On November 16, 2020, the testnet was released for early users to experiment with and report bugs. The protocol officially launched on the Ethereum mainnet on Sunday, December 20, 2020, at 4 pm PST (Monday, December 21, 2020, at 0:00 UTC).[3][4][25]

One hour after launch the total value locked (TVL) in Frax Finance was over $43 million. As of Jan 13, 2021, 100 Million FRAX tokens had been minted, with a collateral ratio of around 85%.[5]

On January 19, 2021, Frax Finance passed Wrapped Bitcoin (WBTC) to become the 5th most liquid token on Uniswap with over $130 million in liquidity.[6]

On February 17, 2021, Frax Finance became the first fractional stablecoin to be listed on Binance. Binance listed Frax Shares in their Innovation Zone with FXS/BTC and FXS/BUSD trading pairs opening on February 18, 2021, 9:00 AM (UTC) and deposits opening earlier.[7]

In January 2022, Frax Finance expanded its collaboration with Chainlink to bring the U.S. CPI data on-chain in support of the Frax Price Index. [11]

On April 29th, 2025, the North Star update marked a significant update to the Frax ecosystem. As part of this upgrade, the Frax Share (FXS) token was renamed to FRAX and designated as the native gas token for the Fraxtal blockchain, replacing frxETH. FRAX also became the sole commodity asset used for network security across the ecosystem.

Overview

Frax V1

Before the inception of the Frax Finance protocol, stablecoins were divided into three different categories: fiat collateralized, overcollateralized with cryptocurrency, and equilibrium. [9]

The Frax protocol is the first stablecoin designed to transition from fully collateralized to varying levels of fractional backing whereby parts of the supply are not backed by any assets but rather minted and bought back by the protocol itself to keep the price of its stablecoin at $1. [8]

The protocol is a two-token system encompassing the stablecoin frxUSD and the Frax token (FRAX, formerly FXS), which accrues seigniorage revenue, fees, and provides governance rights.

The project has also announced a third token, the Frax Bonds token (FXB), to be released at a future date as an interest-bearing token representing debt in the system.

The price of frxUSD, FRAX (formerly FXS), and collateral are all calculated with a time-weighted average price (TWAP) of the Uniswap pair price and the ETH:USD Chainlink oracle. The Chainlink oracle allows the protocol to get the true price of USD instead of an average of stablecoin pools on Uniswap. This allows frxUSD to stay stable against the United States dollar itself, which provides greater resiliency instead of using a weighted average of existing stablecoins only. [8]

Frax V2

Frax V2 expands on the idea of fractional-algorithmic stability by introducing the idea of the "Algorithmic Market Operations Controller" (AMO). An AMO module is an autonomous contract(s) that enacts arbitrary monetary policy so long as it does not change the frxUSD price off its peg. This means that AMO controllers can perform open market operations algorithmically, but they cannot arbitrarily mint frxUSD out of thin air and break the peg. [10]

Frax V3

Frax V3 utilizes AMO smart contracts and permissionless, non-custodial subprotocols as stability mechanisms. The internal subprotocols employed for stability are Fraxlend, a decentralized lending market, and Fraxswap, an automated market maker (AMM) with unique features. As an external stability mechanism, Curve is utilized. Through governance, Frax V3 has the flexibility to seamlessly incorporate future stability mechanisms as they emerge, including additional subprotocols and AMOs. [14][15]

Full exogenous collateralization of frxUSD: The protocol strives to maintain a 100% collateralization ratio (CR) at all times. Starting in V3 and after FIP188, the Frax Protocol aims to achieve this by utilizing AMO smart contracts and specific real-world assets held by partner entities approved by the Frax Governance module (frxGov). The CR of frxUSD stablecoins is calculated based on the value of external collateral held on the Frax balance sheet. This segregated balance sheet serves as collateral to stabilize the market price of frxUSD stablecoins.[16]

Sovereign USD peg: Once the frxUSD stablecoin achieves a 100% collateralization ratio (CR), its peg to the USD will be maintained through a combination of Chainlink oracles and governance-approved reference rates. If the frxUSD CR decreases, AMOs (Algorithmic Monetary Officers) and governance should make efforts to restore the CR to 100% and ensure that the price of frxUSD remains at $1.00, regardless of the prices of other assets like USDC, USDT, or DAI.

Fraxswap

Fraxswap is the first constant product automated market maker with an embedded time-weighted average market maker (TWAMM) designed by Frax Finance. Fraxswap is mainly used for conducting large trades over long periods trustlessly. In June 2022, the Frax Finance team announced the launch of Fraxswap. [15]

Borrow AMM (BAMM)

The Borrow AMM (BAMM) is a borrowing and lending protocol built on top of Fraxswap. It allows users to borrow funds to create leveraged positions or rent out liquidity from an existing Fraxswap pair without relying on external oracles. [10]

Fraxtal

Fraxtal is an EVM-compatible layer 2 rollup chain for Frax Finance, described as a high-performance blockchain optimized for stablecoin scalability and real-time payments. Fraxtal reduces congestion on Ethereum using roll-up technology, which bundles transactions off-chain and compresses data before sending it back to Ethereum. [29] In a January 2024 interview, Sam Kazemian announced the launch of Fraxtal, with the release scheduled for the first week of February 2024.[17][18][19]

The Fraxtal L2 blockchain utilizes the ecosystem's native assets. Following the North Star update, the FRAX token (formerly FXS) became the network's native gas token, replacing frxETH. The ecosystem's stablecoins, such as frxUSD, are central to the chain's operations. The decentralized stablecoin-focused exchange, Curve Finance, has shown its interest in Fraxtal. Curve intends to deploy its exchange functionalities on the new layer 2 blockchain, further solidifying the project's collaborations.[20]

Tokenomics

Frax Token (FRAX)

The Frax Token (formerly Frax Share, FXS) eschews DAO-like active management similar to MakerDAO. The design of the protocol is such that FRAX (formerly FXS) would be largely deflationary in supply as long as frxUSD demand grows.

The token serves as the native gas and base asset of the Fraxtal blockchain. It is issued directly on Fraxtal Layer 1 and follows a fixed, immutable emission schedule. Unlike governance tokens, FRAX (formerly FXS) is categorized as a commodity asset and is not used for protocol decision-making. While wrapped versions may exist on other chains, its origin and primary function remain native to Fraxtal. Per the FRAX (formerly FXS) yearly halvening schedule, the total FRAX emissions halve every 12 months, with the first halvening on December 20, 2021.

veFRAX (formerly veFXS)

veFRAX represents locked FRAX (formerly FXS), used for governance across the Frax ecosystem. Users can lock their FRAX tokens for a period ranging from 1 week to 208 weeks (4 years), with voting power proportional to the amount staked and the duration of the lock. The veFRAX balance is non-transferable and decreases gradually as the lock period nears expiration. [23]

Partnerships

In January 2022, Frax was introduced as a service on Ondo Finance. The partnership will build on Ondo's Liquidity-as-a-Service offering and enable the use of $FRAX (provided by the protocol itself) as liquidity for token issuers. [11]

In December 2021, FRAX partnered with Sacred Finance to bring privacy and stability to Defi. The partnership will allow users to lend FRAX privately and earn yield privately through Sacred. The same month, the Decentralized 3 Pool went live on Convex Finance. This is a triple collaboration between Frax, Fei Protocol, and Alchemix (ALCX). The vision is to make the D3 Curve pool the top choice for farming, saving, and holding decentralized dollar stablecoins. In December, NearPad partnered with Frax Finance to bring FRAX and FXS over to the Aurora and Near ecosystem. [12]

In September 2021, Pangolin and Frax Finance collaborated to bring the FRAX stablecoin to Avalanche. With the collaboration, Pangolin boosts the availability of stablecoins on the Avalanche network for users of Pangolin and provides sufficient liquidity in innovative stablecoins like Frax. They added reward pools for the AVAX-FRAX pair and the AVAX-FXS pair to support liquidity. [13]

In January 2025, Frax Finance introduced a new iteration of its stablecoin, frxUSD, in partnership with BlackRock and Securitize. The updated stablecoin is backed by BlackRock’s USD Institutional Digital Liquidity Fund (BUIDL) and tokenized by Securitize, a firm registered to provide regulated financial services such as brokerage and asset tokenization. The frxUSD stablecoin, formerly known as FRAX, offers direct fiat redemption and aims to align more closely with U.S. financial compliance standards. As part of the arrangement, BUIDL has become a custodied reserve asset for minting and redeeming frxUSD, anchoring the stablecoin to underlying assets like U.S. Treasury bills, cash, and repurchase agreements. [21]

ATW Partners $50 Million Investment in frxUSD

On January 14, 2026, Frax announced a strategic initiative with New York-based investment firm ATW Partners and digital asset custodian BitGo. The partnership includes a commitment from ATW Partners to invest up to $50 million in the frxUSD stablecoin, aiming to bridge traditional finance (TradFi) with the DeFi ecosystem. [29]

Investment and Custody Details

Under the agreement, ATW Partners, via its affiliates and portfolio companies, will deploy the capital into frxUSD. BitGo Bank & Trust will serve as the qualified custodian, holding the frxUSD on behalf of ATW Partners to provide an institutional-grade security framework. The reserves backing the frxUSD are supported by tokenized U.S. Treasury exposure through WisdomTree's WTGXX vehicle on the FraxNet platform. [29]

Strategic Importance

The collaboration is intended to accelerate the institutional adoption of frxUSD by providing a secure and compliant entry point for traditional financial entities. The involvement of BitGo as a qualified custodian addresses a key requirement for institutional investors by providing security and transparency. A representative from ATW Partners noted the goal is to "bring institutional participation and new real-world use cases for frxUSD," such as B2B payments. Frax founder Sam Kazemian commented that the initiative shows "how modern financial institutions use stablecoins... unlocking the superior speed and flexibility of stablecoins over traditional finance." [29]

Binance Listing and Fraxtal Network Integration

On January 15, 2026, Frax announced that the cryptocurrency exchange Binance would list its new ecosystem token, FRAX, and integrate its proprietary Fraxtal network. The development was part of Frax's strategy to evolve from a single protocol into a "full-stack stablecoin operating system." [26]

Token Upgrade: FXS to FRAX

As part of the announcement, the Frax Shares (FXS) token was upgraded to the new, singular ecosystem token named FRAX. Binance committed to managing the migration of all existing FXS positions on its platform to the new FRAX token. Frax founder Sam Kazemian stated the change was to "reflect what Frax has become: a scalable stablecoin operating system, not just a single protocol." The new FRAX token is designed to capture value from the entire Frax ecosystem, including the frxUSD stablecoin, the Fraxtal blockchain (which uses FRAX for gas fees), and FraxNet, an account-based platform. [26]

Fraxtal Network Integration

Binance also added support for Fraxtal, Frax's Ethereum-compatible blockchain. Frax described the integration as a "vote of confidence" in the network's quality and long-term utility. Fraxtal is a high-performance chain designed to serve as the execution and settlement layer for frxUSD and other stablecoin-related activities, such as payments and treasury management. Kazemian commented that the integration was a "strong signal that Fraxtal has meaningful purpose and lasting value." [26]

FXS to FRAX Token Swap on Bybit

On December 30, 2025, Frax Finance announced an upgrade and rebranding of its governance token, Frax Share (FXS), to a new ecosystem token named Frax (FRAX). The move was part of a strategic pivot to establish the new FRAX token as the native gas token for Fraxtal, the project's Layer 2 network. The upgrade was intended to position the FRAX token at the center of the ecosystem's operations and give holders exposure to the growth of the frxUSD stablecoin. [27]

The cryptocurrency exchange Bybit announced it would support the migration. Bybit managed the technical aspects of the token swap, automatically converting all user-held FXS tokens to the new FRAX token at a 1:1 ratio. The exchange suspended deposits, withdrawals, and trading for FXS on January 6, 2026, and enabled deposits, withdrawals, and spot trading for the new FRAX/USDT pair on January 12, 2026, ensuring a seamless transition for its customers. [28]

Aave V4 Integration

On April 6, 2026, Frax Finance's stablecoin, frxUSD, launched as a default borrowable asset on the Aave V4 protocol. This integration, which made frxUSD available from the protocol's first day, enhances the stablecoin's utility and liquidity within the DeFi ecosystem. To support the launch, Frax governance approved deploying up to $27.5 million to bolster liquidity for frxUSD on Aave V4 and its associated Morpho vaults, as well as to maintain the stablecoin's peg. [31]

The integration leverages Aave V4's "hub-and-spoke" architecture, which unifies liquidity across various borrowing environments. Frax founder Sam Kazemian described the day-one launch as a "strong signal of the secureness with which we built frxUSD," while Aave Labs founder Stani Kulechov noted the importance of "strong stablecoin participants" for DeFi's next phase. frxUSD is a fully collateralized, fiat-redeemable stablecoin backed by real-world assets like tokenized U.S. Treasuries. [31]

Frax 2030 Vision Upgrade

The Frax ecosystem is undergoing significant changes to strengthen its position as a leader in DeFi. These updates include token ticker changes, the introduction of new infrastructure, and the evolution of Frax’s Layer 2 solution, Fraxtal, to meet the demands of a rapidly advancing blockchain landscape.

Token Ticker Changes

Frax is transitioning its flagship stablecoin, FRAX, to frxUSD immediately after governance approval. This change is more than cosmetic; incorporating “USD” into the name aims to attract the next wave of crypto users by making the stablecoin more accessible and familiar. With a $600M market cap, frxUSD will feature advanced capabilities such as direct fiat redemptions through Paxos. Frax also plans to secure access to a US Federal Reserve Master Account (FMA) via its partner FinresPBC, further enhancing its stability and security. The savings vault product, sFRAX, will transition to sfrxUSD, maintaining its status as one of the best risk-adjusted yield options in DeFi.

Meanwhile, Frax’s governance token, FXS, will be rebranded as FRAX with the Fraxtal North Star Hard Fork in February. This change reflects FXS’s evolution from a share token to the currency of Fraxtal, a top-tier Layer 2 (L2) ecosystem. Until the hard fork, FXS will be referred to as "FRAX fka FXS." veFXS will also transition to veFRAX, preserving its governance power and revenue-sharing mechanics.

Crypto Strategic Reserve (CSR)

Frax is establishing an on-chain Crypto Strategic Reserve (CSR) denominated in BTC and ETH. This reserve will become one of the largest balance sheets in DeFi, solidifying Frax’s reputation as the “MicroStrategy of DeFi.” The CSR will reside on Fraxtal, directly contributing to the ecosystem's total value locked (TVL) as it grows. Governance by veFRAX stakers will determine the specific weights and mechanics of the CSR, providing transparency and community participation in shaping its future.

Frax Burn Engine

To ensure long-term value and scarcity, Frax is introducing the Frax Burn Engine. This immutable infrastructure will include innovations like the Frax Name Service (FNS) and EIP1559-style base fees. These mechanisms will actively burn FRAX over time, counteracting emissions and increasing its scarcity.

Fraxtal North Star Hard Fork

The Fraxtal North Star Hard Fork represents a pivotal moment for the ecosystem, focusing on decentralization, speed, and AI integration. Fraxtal, an Optimistic Rollup inheriting decentralization from Ethereum, will achieve high-throughput, real-time block processing, positioning it alongside the fastest blockchains like Sei and Monad.

The fork will also introduce AI-specific features, such as "Proof of Inference" and the AIVM (Artificial Intelligence Virtual Machine), developed in partnership with IQ.wiki. These capabilities are designed to meet the future demands of blockchain technology, where AI-driven agents are expected to dominate usage.

As part of the hard fork, the Fraxtal ecosystem will transition from frxETH to FRAX as its gas token. This change will result in the instant conversion of frxETH gas to FRAX at the current exchange rate, generating significant buy pressure for FRAX. Additionally, Frax will release $FXTL, a new blockspace incentive token tied to Fraxtal’s infrastructure.

Frax.com Universal Interface (¤UI)

To streamline user interactions, Frax.com will relaunch as the Frax Universal Interface (¤UI). This overhaul simplifies DeFi processes, allowing users to borrow, swap, and send tokens in just a few clicks. The ¤UI will be supported by exclusive partners, including Odos Routing for real-time transaction optimization and Halliday Onramping for seamless fiat-to-crypto access worldwide.

Future plans for ¤UI include the development of a Frax mobile wallet and further integration of AI to enhance user experience. For advanced DeFi operations, the existing professional interface will remain available.

See something wrong?

Wiki Powered byIQ

Categories

Tags

Verification

Events

Views

14,513

Categories

Tags

Verification

Events

Views

14,513

Average Rating

Based on over 1 ratings

How was your experience?

Give this wiki a quick rating to let us know!

Edited By

On July 14, 2026. 23:21 UTC

Edit summary:

Updated wiki content