0% read

Tokenization

Tokenization

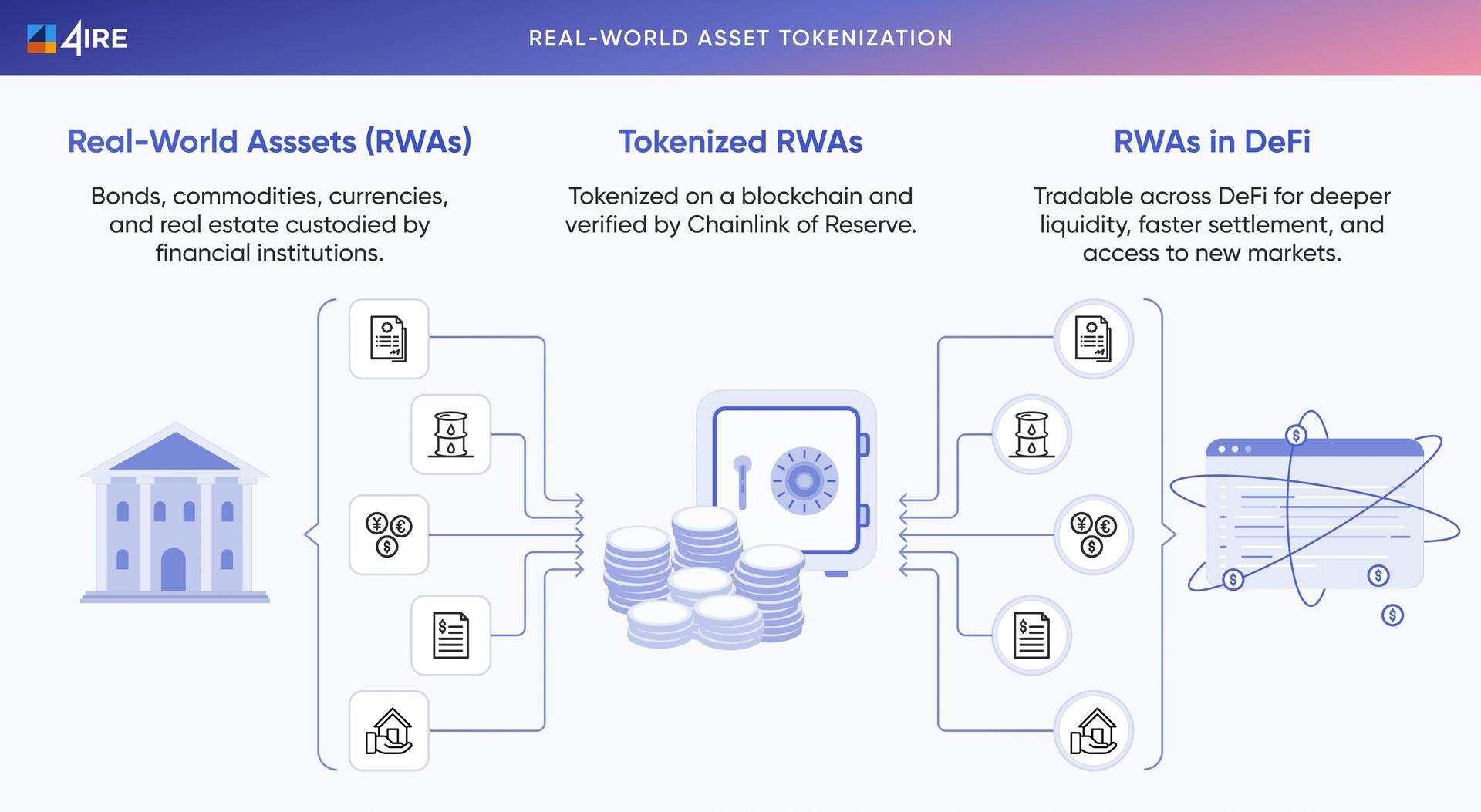

Tokenization is the process of converting the rights to a tangible or intangible asset into a unique digital representation, known as a token, on a blockchain or other distributed ledger technology (DLT). These tokens can represent ownership of a wide variety of assets, including real estate, art, stocks, bonds, intellectual property, and carbon credits. The process is also frequently referred to as Real-World Asset (RWA) tokenization, as it aims to bring traditional off-chain assets into the on-chain digital economy. [1] [2]

Overview

The primary objective of tokenization is to merge the reliability and regulatory frameworks of traditional finance (TradFi) with the efficiency, transparency, and innovation of decentralized finance (DeFi). [3] By representing real-world assets as digital tokens, they become more divisible, allowing for fractional ownership, and can be managed and traded more easily in a global, 24/7 market. This can increase liquidity for assets that are traditionally difficult to sell, such as private equity or commercial real estate. [4] A survey conducted by BNY Mellon and Celent found that 97% of institutional investors believe tokenization will have a significant impact on asset management. [4]

The potential scale of the tokenized asset market has attracted significant attention from major financial analysts. Boston Consulting Group (BCG) projected the market could reach 4 trillion to 2 trillion by 2030, a figure that excludes native cryptocurrencies and major stablecoins. [5]

Historical Development

Pre-Blockchain Origins

The concept of tokenization predates blockchain technology, with its earliest applications emerging in the financial services industry during the 1970s. This initial form of tokenization was primarily a data security method used to protect sensitive information. It involved converting data like credit card or Social Security numbers into a non-sensitive string of alphanumeric characters, or a "token," to prevent fraud. While visually similar, this data protection method has a fundamentally different purpose than the asset-ownership representation enabled by modern blockchain technology. [6] [5]

Blockchain-Era Milestones

The application of blockchain to tokenization shifted the focus from data security to asset representation, leading to a series of key milestones demonstrating growing institutional adoption.

- 2020: J.P. Morgan established Onyx, a division dedicated to wholesale payments and tokenized assets on a permissioned blockchain platform. Around the same time, German multinational Siemens issued its first digital bond on a blockchain, showcasing an early use case by a major industrial firm. [2]

- 2023: Larry Fink, CEO of BlackRock, publicly endorsed the technology, stating that "the next generation for markets, the next generation for securities, will be tokenization of securities," which signaled strong institutional interest. [2]

- March 2024: BlackRock launched the USD Institutional Digital Liquidity Fund (BUIDL) on the Ethereum network in partnership with Securitize. This was a landmark event, as it created a tokenized money market fund from the world's largest asset manager. [1]

- December 2025: The Depository Trust & Clearing Corporation (DTCC), a central pillar of U.S. financial market infrastructure, received a No-Action Letter from the Securities and Exchange Commission (SEC) authorizing its plan to offer a tokenization service. The DTCC subsequently announced a partnership with Digital Asset to use the Canton Network for this service, which is anticipated to launch in the second half of 2026. [3]

The Tokenization Process

Tokenizing a real-world asset involves a multi-stage process that combines legal, financial, and technical elements to bridge the off-chain and on-chain worlds. [1]

- Asset Selection and Due Diligence: An issuer identifies a specific asset for tokenization. A thorough vetting process is conducted to determine its value, verify legal ownership, and ensure it is free from encumbrances. [2]

- Legal Structuring: The physical asset is typically placed into a legally distinct structure, often a Special Purpose Vehicle (SPV) or a trust. This "legal wrapper" holds legal title to the asset, isolating it from the issuer’s other financial risks and ensuring that token holders have a legally enforceable claim to the asset. [1]

- Token Issuance and Smart Contract Engineering: A smart contract is developed and deployed on a selected blockchain. This contract governs the behavior of the tokens, including rules for issuance, transfer, and compliance. Using this smart contract, a specific number of digital tokens are created, or "minted," to represent ownership shares in the underlying asset.

- Distribution and Secondary Trading: The newly minted tokens are offered to investors, often through a Security Token Offering (STO) on a regulated platform. Following the initial sale, these tokens can be traded on secondary markets, which can operate globally on a 24/7 basis. [1]

- Custody and Asset Management: Secure custody solutions are required for both the off-chain physical asset (e.g., held in a vault or by a qualified custodian) and the on-chain digital tokens. Institutional-grade digital wallets, such as those using Multi-Party Computation (MPC), are often used to manage the private keys that control the tokens, eliminating single points of failure. [2]

Core Technology and Infrastructure

Tokenization is enabled by a stack of Web3 technologies and requires a robust support infrastructure to function effectively at scale. [5]

Underlying Technologies

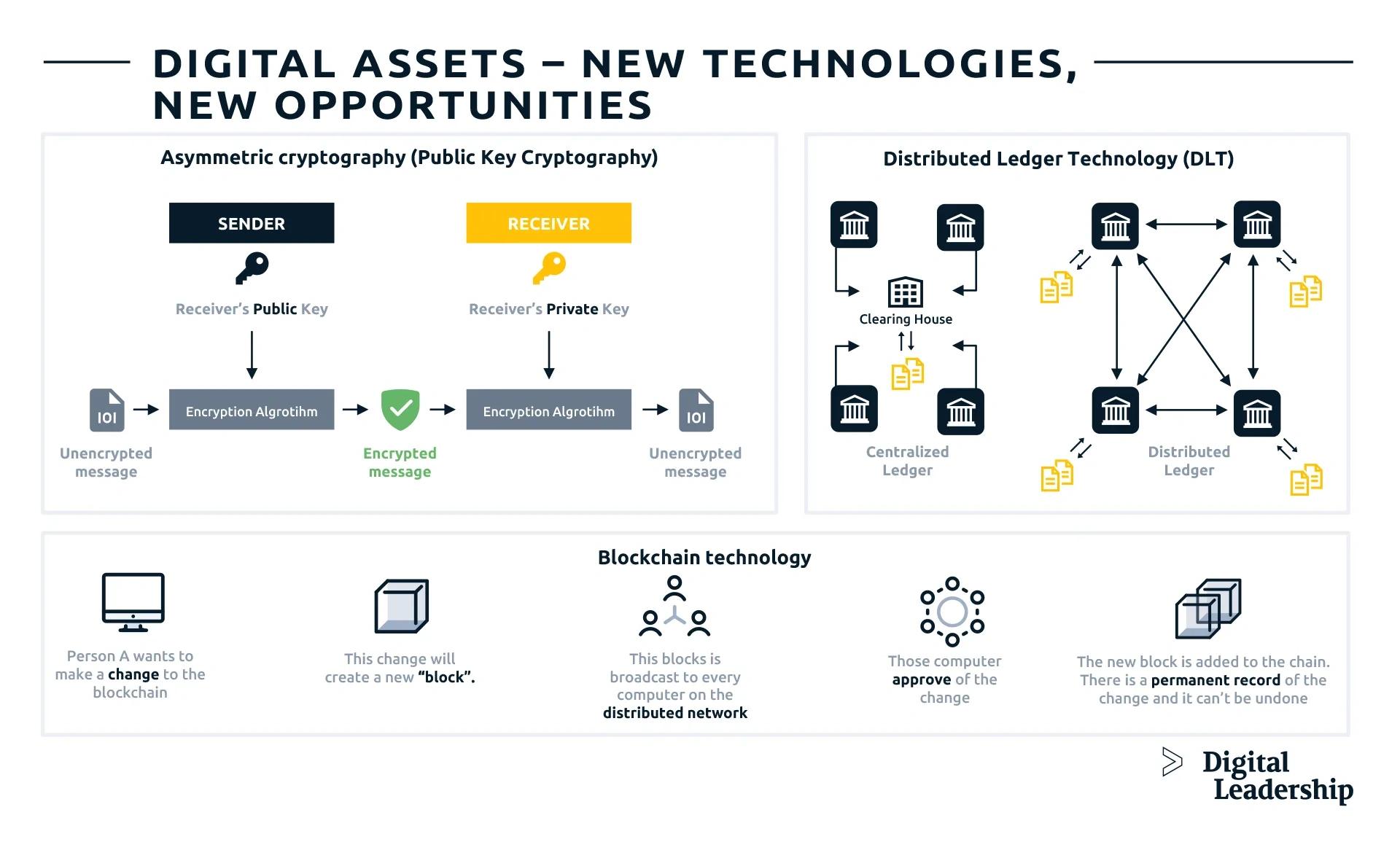

- Blockchain: This serves as the decentralized and immutable digital ledger that records all token transactions and ownership balances. While public blockchains like Ethereum are common, many financial institutions are exploring tokenization on private or permissioned blockchains, which offer greater control over participation and privacy.

- Smart Contracts: These self-executing programs are stored on the blockchain and automatically enforce the terms of an agreement. In tokenization, they govern the entire lifecycle of a token, automating tasks like dividend distribution, interest payments, compliance checks, and voting based on predefined rules. [5]

- Digital Wallets: Investors require a digital wallet to securely store, manage, and transact with their tokenized assets. [5]

Essential Support Infrastructure

For tokenized assets to function properly and interact with external systems, they rely on several critical services:

- Data Oracles: Oracles are services that securely fetch external, real-world data and deliver it to smart contracts on the blockchain. This data is essential for dynamic tokenized assets, providing information such as current asset prices, interest rates, or verification of reserves, which can trigger on-chain functions. [4]

- Cross-Chain Interoperability: To avoid liquidity being trapped on a single blockchain, interoperability protocols are needed to allow tokens and data to move securely between different public and private chains. Protocols like the Cross-Chain Interoperability Protocol (CCIP) are being explored by institutions like Swift and the DTCC to create a more connected ecosystem. For native tokens, standards such as the Omnichain Fungible Token (OFT) allow a token's liquidity to be unified across multiple blockchains rather than fragmented. [4] [7]

- Proof of Reserve (PoR): For tokens backed by off-chain assets (e.g., stablecoins backed by fiat currency or tokens backed by gold), Proof of Reserve systems provide on-chain transparency. They use oracles to autonomously audit and verify that the issuer holds sufficient reserves to back the circulating supply of tokens, enhancing trust and security. [4]

Types of Tokens

Tokens can be classified based on their function, the nature of the underlying asset, and their technical standard.

By Functionality

- Security Tokens: These represent a traditional financial investment, such as equity in a company, a voting right, or a share of profits. They are subject to securities regulations and can be programmed with complex rules. [6]

- Tokenized Securities: Distinct from security tokens, these act as a more straightforward digital "stand-in" for a traditional security like a stock or bond. Their primary purpose is to improve the liquidity and accessibility of the underlying security without adding the unique programmable features of a native security token. [6]

- Utility Tokens: These provide users with access to a specific product or service on a blockchain network, such as paying for transaction fees, powering network operations, or granting governance rights in a Decentralized Autonomous Organization (DAO). [6]

- Currency Tokens: This category includes cryptocurrencies and stablecoins (e.g., USDT, USDC) designed primarily as a medium of exchange. [6]

By Asset Nature

- Fungible Tokens: These tokens are identical and interchangeable. Each unit holds the same value and properties as any other unit, making them ideal for representing currency or shares in a fund. [6]

- Non-Fungible Tokens (NFTs): Each NFT is unique, provably scarce, and has a distinct, traceable history of ownership. This makes them suitable for representing one-of-a-kind assets like a specific piece of art, a collectible, or a property deed. [6]

By Technical Standard

- ERC-20: The most common standard on Ethereum for creating fungible tokens.

- ERC-721: The standard for creating non-fungible tokens on Ethereum.

- ERC-1400 / ERC-3643: These are security token standards designed with built-in compliance features, allowing issuers to program transfer restrictions and other regulatory rules directly into the token. [1]

Benefits

Tokenization offers several advantages over traditional financial systems by leveraging the inherent properties of blockchain technology.

- Increased Liquidity and Fractional Ownership: Tokenization allows large, illiquid assets like commercial real estate to be divided into smaller, affordable fractions. This democratizes access for a wider range of investors and can unlock value by creating a more active trading market. [6]

- Faster Transactions and Real-Time Settlement: Blockchain transactions can settle in near-real-time (T+0), a significant improvement over the traditional multi-day settlement cycles (e.g., T+2) in stock markets. This frees up capital and reduces counterparty risk. [4]

- Enhanced Transparency and Provability: Every transaction and change in ownership is recorded on an immutable blockchain ledger, providing a transparent and easily auditable history of the asset. This "single source of truth" reduces the potential for fraud and disputes. [6]

- Operational Efficiency and Reduced Costs: Smart contracts automate manual processes like compliance, dividend payouts, and settlement, reducing the need for costly intermediaries such as brokers and transfer agents. [5]

- Programmability and Composability: Tokens can be programmed with complex logic. Their ability to seamlessly interact with other applications on the same network (composability) enables the creation of novel financial products, such as using a tokenized bond as collateral on a DeFi lending platform. [5]

- Global Accessibility: As digital assets on a blockchain, tokens can be accessed and traded by a global pool of investors 24/7, breaking down geographical barriers and creating more unified capital markets. [4]

The Intersection of AI and Tokenization

The convergence of artificial intelligence (AI) and tokenization has created new possibilities for autonomous economic agents and decentralized commerce. This synergy enables AI to move from being a passive tool to an active participant in on-chain economies. [8]

Autonomous AI Agents as Tokenized Assets

An emerging frontier is the tokenization of AI agents themselves, allowing them to own assets, execute transactions, and participate in governance autonomously. The core idea is to give an AI agent its own unique token, which represents its value, capabilities, and governance rights, effectively turning it into a self-sustaining on-chain entity. [8]

Venture capital firm Andreessen Horowitz (a16z) predicted in late 2024 that a key trend for 2025 would be the development of AI agents capable of custodying their own crypto wallets, enabling them to autonomously sign keys and actively participate in crypto markets. [9] Projects like IQ AI's Agent Tokenization Platform (ATP), launched in collaboration with Frax and NEAR Protocol in February 2025, aim to provide the infrastructure for this vision. ATP allows for the creation of tokenized AI agents on the Fraxtal blockchain that can leverage DeFi protocols for lending, borrowing, and trading. [8]

This model depends on a technical stack comprising Large Language Models (LLMs) as the "brain," frameworks for deploying agents, blockchains for execution, and interoperability protocols to allow agents to operate across different chains. [7]

AI-Driven Commerce and Marketplaces

AI agents are also poised to transform commerce by leveraging tokenized physical assets. In this model, AI serves as an abstraction layer that simplifies user interaction with complex Web3 systems. For example, an AI agent could aggregate product data from various siloed marketplaces, represent these goods as tokens on-chain, and facilitate trustless transactions via smart contracts. [10] This approach aims to create an open and liquid global marketplace for both physical and digital goods, breaking down the walled gardens of traditional e-commerce platforms. [10]

Future Outlook and Emerging Trends

As the infrastructure for tokenization matures, its applications are expected to expand into new and unconventional asset classes.

Tokenization of Government Bonds

Analysts predict that nation-states will begin to explore the tokenization of government bonds. Putting government debt on-chain would create a government-backed, interest-bearing digital asset that could serve as high-quality collateral in DeFi ecosystems. This would differ from a Central Bank Digital Currency (CBDC) by avoiding many of the surveillance concerns associated with CBDCs. The U.K. treasury has already expressed interest in "digital gilts," indicating movement in this direction. [9]

Tokenization of Unconventional Assets

Technological advancements are expected to lower the costs associated with tokenization, making it feasible to tokenize a wider range of previously untapped assets. Examples include personal or biometric data, where individuals could tokenize and capitalize on their own information in a secure and decentralized manner. This could create new income streams and redefine personal data ownership in the digital age. [9]

See something wrong?

Average Rating

No ratings yet, be the first to rate!

How was your experience?

Give this wiki a quick rating to let us know!

Edited By

On June 18, 2026. 14:30 UTC

Edit summary:

Expanded summary and updated Glossary title and ID